Europe’s drive to adopt synthetic sustainable aviation fuels (e-SAF) is confronting a critical physical limitation: the availability of renewable electricity.

According to recent analysis by the International Air Transport Association (IATA), e-SAF—defined as a renewable fuel of non-biological origin—requires 20 to 40 megawatt-hours (MWh) of renewable electricity per tonne of fuel produced. Scaled to national production targets, this translates into an annual electricity demand of 0.7 to 10 terawatt-hours (TWh) by 2030, depending on the country.

These figures reveal a structural tension at the heart of Europe’s aviation decarbonisation strategy. While policy frameworks increasingly mandate SAF blending and set long-term net-zero targets, the upstream electricity infrastructure may not yet be capable of supplying sufficient renewable power at competitive prices.

Europe at the Forefront of e-SAF Development

Europe has positioned itself as a global leader in early e-SAF deployment. Current plans envision 1.5 million tonnes of e-SAF capacity by 2030, representing roughly 80% of global projected capacity. Yet the continent faces significant disparities in renewable electricity availability across member states.

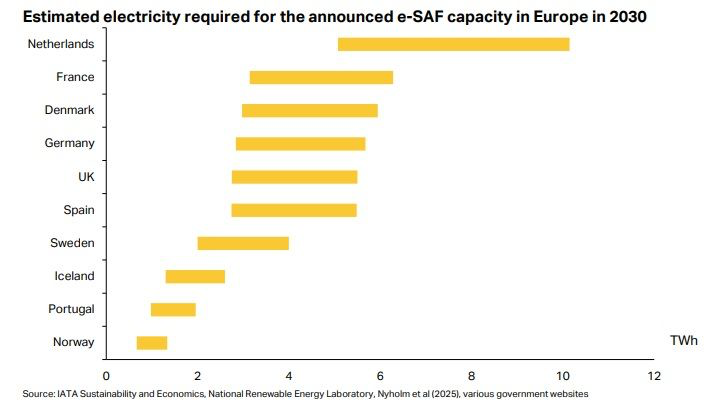

Countries such as the Netherlands, Germany, and the UK have announced ambitious e-SAF targets despite renewable energy accounting for just over half of total electricity generation in 2024. IATA estimates that the Netherlands’ projected 2030 e-SAF production could consume up to 31% of its 2024 renewable grid capacity, illustrating the scale of the challenge: without rapid expansion in renewable generation, production targets risk outpacing supply.

By contrast, nations like Norway, Portugal, and Iceland, where renewables already supply around 90% of the electricity mix, face fewer short-term constraints, though long-term e-SAF expansion will still depend on continued growth in generation capacity. IATA’s projections rank the Netherlands at the top of the anticipated electricity demand scale, followed by France, Denmark, Germany, and the UK, with Spain and Sweden in the mid-tier, and Norway and Portugal requiring comparatively smaller volumes. This disparity underscores how national energy structures will directly influence the feasibility of local e-SAF production.

The 2050 Challenge

Looking further ahead, the pressure intensifies. To achieve global net-zero aviation by 2050, IATA estimates approximately 205 million tonnes of e-SAF will be needed. Europe’s 1.5 million tonnes planned for 2030 represents only an initial step rather than a decisive shift.

For cargo operators in particular, the implications are significant. Widebody freighters and long-haul freight networks have limited alternatives to liquid fuels; battery-electric or hydrogen propulsion remains technologically distant for heavy cargo operations. SAF, including synthetic e-SAF, therefore emerges as one of the few scalable decarbonisation pathways in the medium term.

Yet synthetic fuel production is fundamentally an energy conversion process. Economics are highly sensitive to renewable electricity prices and electrolyser efficiency. Scarce or costly power directly increases production costs, limiting airline uptake—even in markets with mandated blending requirements.

As Europe continues to pursue e-SAF at scale, aligning renewable energy expansion with aviation fuel targets will be essential to meet both climate objectives and operational viability for airlines and cargo operators alike.

{kind=link}