The ongoing conflict in the Middle East is placing mounting pressure on global airfreight markets, as escalating jet fuel prices, constrained capacity, and geopolitical uncertainty combine to reshape pricing dynamics and supply chain strategies.

Data and analysis from Xeneta indicate that, while the sector has demonstrated short-term resilience, underlying risks are intensifying. Airlines, freight forwarders, and shippers are working collaboratively to maintain cargo flows and protect service levels, even as operational costs rise sharply.

In the immediate term, demand for air cargo services has remained stable. Shippers continue to prioritise speed and reliability to safeguard market share and customer commitments, absorbing higher transport costs where necessary. This collective response has helped stabilise market conditions despite external volatility.

However, industry observers caution that this stability may be temporary.

“There is considerable uncertainty surrounding the market outlook,” said Niall van de Wouw, Chief Airfreight Officer at Xeneta. “At the same time, we are witnessing greater transparency and alignment between stakeholders, alongside a shared recognition that the challenges posed by the conflict must be managed collectively.”

Rising Costs and Tight Capacity Reshape Pricing

The most immediate impact of the conflict has been a pronounced increase in airfreight rates. Higher jet fuel costs, reduced regional capacity, and the introduction of war-risk surcharges are driving pricing upward across multiple trade lanes.

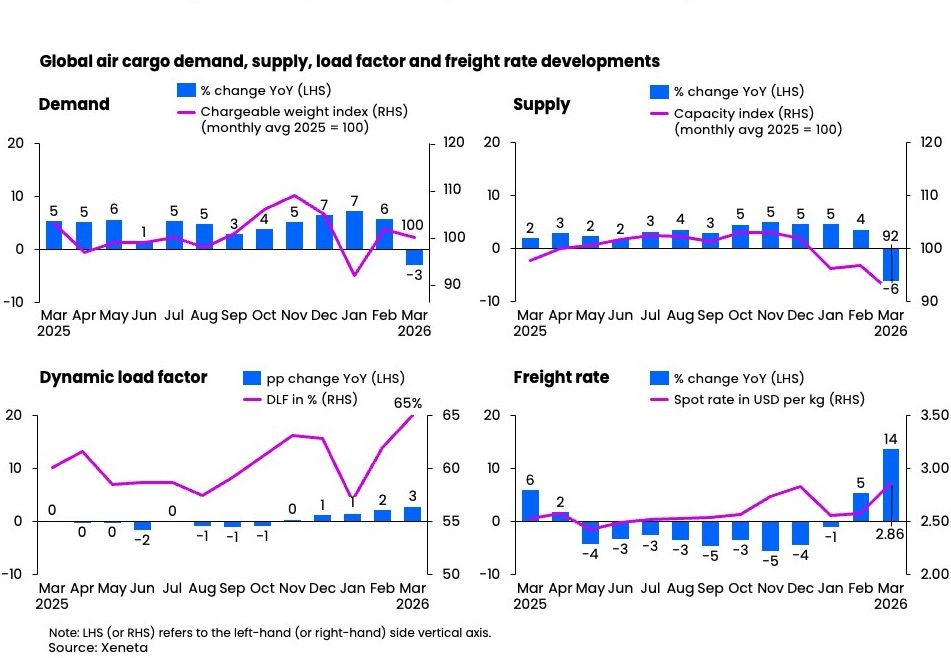

Global air cargo demand declined by 3% year-on-year in March, while available capacity fell by 6%, resulting in tighter utilisation. Xeneta’s dynamic load factor reached 65%, reflecting increased pressure on available space.

Spot rates have risen to $2.86 per kilogram—the highest level recorded since December 2024—surpassing typical peak-season benchmarks.

In the Middle East, air cargo capacity remains approximately 30% below pre-conflict levels, further exacerbating supply constraints and limiting routing flexibility.

Disruption Extends Across Global Trade Corridors

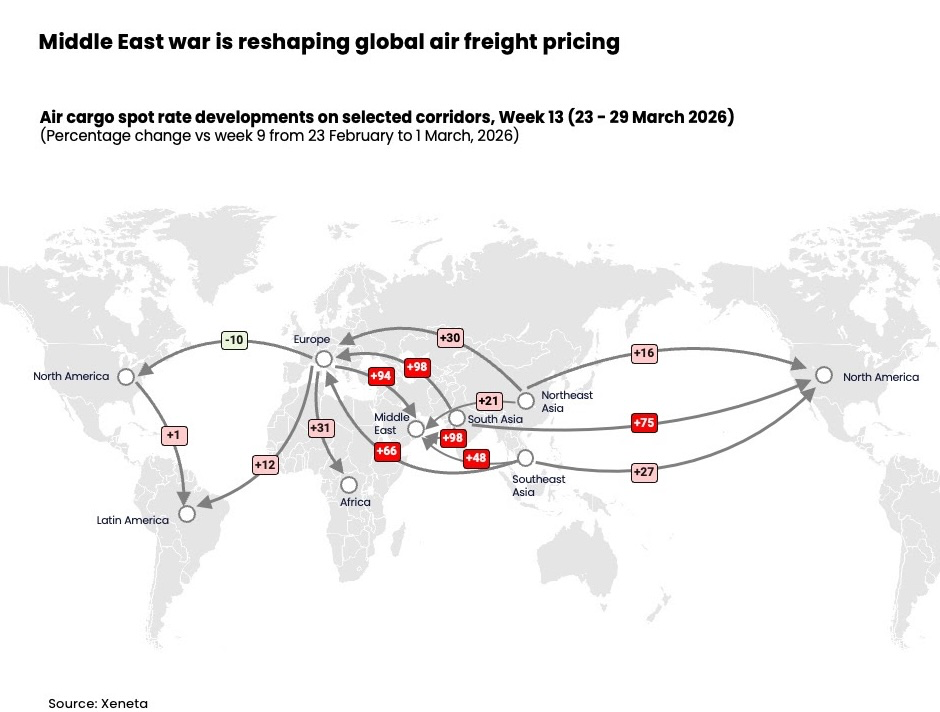

The effects of the conflict are no longer confined to the Middle East. Given the region’s strategic importance as a global transit hub—particularly for Asia–Europe and South Asia–Americas routes—disruptions are cascading across international airfreight networks.

Routes from South Asia and Southeast Asia to the Middle East have experienced the most significant volatility, with spot rates increasing between 50% and 100% in the final week of March compared to the previous month.

This escalation reflects a convergence of structural pressures, including:

- Heavy reliance on Middle Eastern carriers

- Severe capacity shortages

- Elevated fuel costs

- Additional war-risk surcharges

The impact has extended further:

- Asia–Europe corridors have seen sustained rate increases, particularly from South and Southeast Asia

- Europe–Africa rates have risen by 31%, underscoring dependence on Middle Eastern hubs

- Asia–North America routes have recorded mid- to high double-digit increases, with South Asia lanes rising by approximately 75%

By contrast, Northeast Asia–Europe routes have remained comparatively stable, supported by the deployment of additional direct flights that bypass affected transit regions.

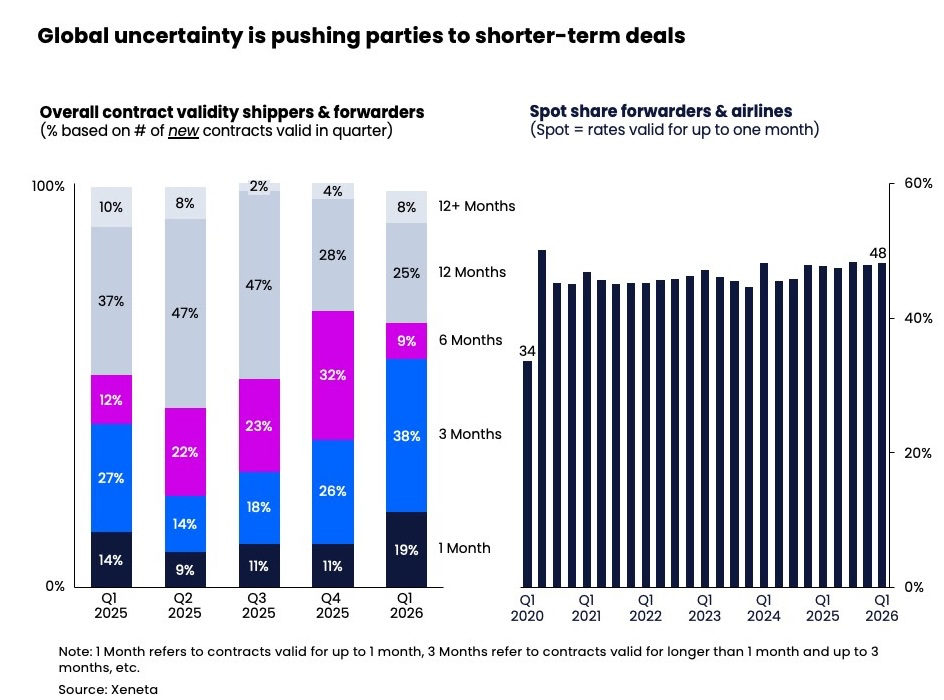

Shippers Shift Toward Short-Term Contracting

In response to ongoing volatility, shippers are increasingly favouring short-term agreements over long-term contracts. Three-month deals have become more prevalent during the first quarter, reflecting a desire for flexibility amid rapidly changing market conditions.

Xeneta has advised delaying long-term tenders, citing limited visibility on future pricing and capacity trends. The shift toward shorter commitments has compressed rate validity periods and contributed to greater reliance on the spot market.

In March, 52% of global air cargo volumes moved under spot rates, approaching levels observed during the early stages of the COVID-19 pandemic.

Divergent Trends Across Key Markets

While many corridors are experiencing upward rate pressure, some markets are showing signs of stabilisation or decline.

Europe–North America spot rates fell by approximately 10% in late March, supported by increased belly cargo capacity as summer passenger schedules resumed. Meanwhile, North America–Latin America rates remained broadly stable, and Europe–Latin America rates rose by around 12% due to capacity adjustments.

Longer-term rate trends suggest a more measured outlook. On Asia–North America routes, rates for contracts exceeding one month increased only marginally, as external factors—including trade policies and weakening demand—continue to exert downward pressure.

Outlook Dependent on Duration of Conflict

Although airfreight has historically acted as a critical enabler during periods of disruption, the current crisis presents distinct challenges. The sector’s exposure to fuel price volatility and its reliance on Middle Eastern transit infrastructure make it particularly vulnerable.

According to Xeneta, the market is currently experiencing a supply-side shock. However, a prolonged conflict could trigger a broader demand contraction, particularly if rising energy costs contribute to inflationary pressures and slower global economic growth.

Short-term gains may emerge as disruptions in ocean freight push cargo toward air transport. However, such shifts are likely to be temporary and insufficient to offset longer-term risks.

Ultimately, the trajectory of the airfreight sector will be determined by the duration and severity of the conflict. While the industry has demonstrated resilience and coordination in the face of immediate disruption, sustained instability could fundamentally alter demand patterns and pricing structures in the months ahead.

{kind=link}