The ongoing Middle East conflict is driving significant shifts in global air cargo capacity, with key Gulf hubs experiencing sharp declines while alternative gateways begin to absorb displaced volumes.

New analysis from Aevean highlights the extent of disruption across major airports, underscoring the region’s central role in global airfreight connectivity and the far-reaching implications of ongoing geopolitical instability.

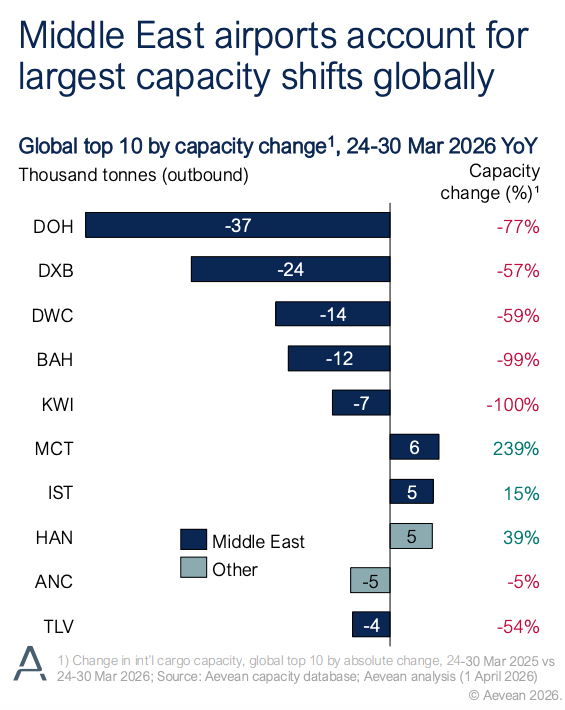

Gulf Hubs Record Sharp Capacity Declines

Airports across the Middle East have borne the brunt of capacity reductions, particularly in outbound cargo volumes. Among the most affected is Hamad International Airport in Doha, a critical hub for Qatar Cargo, widely regarded as the world’s largest cargo airline.

In the week ending 30 March, Doha recorded a year-on-year decline of 37,000 tonnes in outbound cargo capacity—a drop of 77%—marking one of the most significant contractions globally.

Other major Gulf hubs have experienced similarly steep declines:

- Dubai International Airport (DXB) saw capacity fall by 24,000 tonnes, down 57% year-on-year

- Al Maktoum International Airport (DWC) recorded a reduction of 14,000 tonnes, representing a 59% decline

- Bahrain International Airport experienced a drop of 12,000 tonnes

- Kuwait International Airport reported a decrease of 7,000 tonnes

These figures reflect the combined impact of airspace restrictions, operational disruptions, and rising fuel costs, all of which have constrained airline capacity and forced network adjustments.

Partial Recovery and Network Reconfiguration

Despite the sharp decline in capacity, there are early signs of operational recovery. Qatar Cargo has begun gradually reinstating freighter services, announcing a resumption of flights from late March to a broad network spanning Asia, Africa, Europe, and the Americas.

This includes destinations across Vietnam, China, Thailand, South Korea, Nigeria, Kenya, Germany, the Netherlands, Belgium, the United States, Brazil, Ecuador, and Panama—indicating efforts to rebuild connectivity and restore cargo flows through alternative routings.

Secondary Hubs See Capacity Gains

While overall capacity in the region remains under pressure, some airports are emerging as beneficiaries of shifting traffic patterns.

Muscat International Airport and Istanbul Airport have both recorded increases in outbound cargo capacity, as airlines reroute services to avoid disrupted airspace and maintain network continuity.

According to Aevean, these gains are significant in relative terms, though they remain insufficient to offset the substantial losses recorded at primary Gulf hubs.

Meanwhile, Abu Dhabi International Airport has demonstrated relative resilience, with capacity declining by just 3% year-on-year—performing comparatively well given the broader regional disruption.

Global Capacity Under Pressure, but Stabilising

At a global level, the air cargo market is showing signs of stabilisation following an initial sharp downturn. Aevean’s latest data indicates that worldwide cargo capacity is currently just 2% below levels recorded during the same period last year.

This marks a notable recovery from the peak of the crisis, when capacity had fallen by approximately 20% year-on-year amid widespread airspace closures across the Middle East.

Nevertheless, structural pressures persist. Rising jet fuel prices—exacerbated by the conflict—continue to weigh on airline operating costs, while ongoing geopolitical uncertainty is limiting the pace of recovery.

Industry Outlook: Volatility to Persist

Aevean’s analysis underscores the extent to which Middle Eastern hubs function as critical nodes in global airfreight networks. Disruptions in the region are not only affecting local capacity but also reshaping flows across intercontinental trade lanes.

“Airports across the Middle East account for the largest capacity shifts seen anywhere in the world,” said Maarten Wormer, Head of Consulting at Aevean, noting that while some markets are experiencing growth, the overarching trend remains one of constrained capacity.

As airlines continue to adjust networks and explore alternative routing strategies, the redistribution of cargo flows is expected to persist in the near term. The pace and scale of recovery will largely depend on the duration of the conflict, fuel price stability, and the restoration of normal airspace operations.

For now, the global air cargo market remains in a state of recalibration—balancing resilience and adaptability against an evolving geopolitical backdrop.

{kind=link}