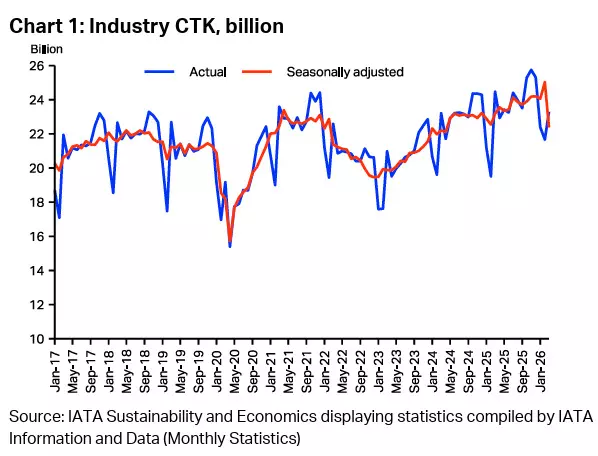

Global air freight markets experienced a notable contraction in March 2026, with cargo tonne-kilometres (CTK) declining 4.8% year-on-year, as geopolitical disruption in the Middle East, elevated fuel costs, and seasonal softness combined to create one of the most complex operating environments in recent years.

According to the latest monthly market analysis, international air cargo traffic was more heavily impacted, falling 5.5% year-on-year, reflecting the disproportionate effect of network fragmentation on cross-border trade flows and long-haul connectivity.

Middle East Collapse Drives Global Downturn

The most severe disruption originated in the Middle East, where cargo volumes plummeted 54.3% year-on-year, marking the region as the primary drag on global airfreight performance.

The decline was driven by restricted airspace operations, rerouting of long-haul services, and reduced hub connectivity, which collectively removed a significant portion of global transit capacity from the network.

The breakdown in Gulf hub efficiency had a cascading effect across Asia–Europe and Europe–Asia flows, where carriers were forced to adopt longer routings, increasing fuel consumption, transit times, and operational complexity.

Industry observers note that the scale of the contraction in the Middle East outweighed gains in all other global regions combined, underscoring the region’s critical role in intercontinental air cargo distribution.

Regional Performance: Growth Outside the Gulf Partially Offsets Losses

Outside the Middle East, global performance remained mixed but comparatively resilient.

Africa recorded the strongest growth at 7%, benefiting from rerouted cargo flows and increased utilisation of alternative routing structures bypassing disrupted Gulf corridors.

Asia Pacific, Europe, and Latin America and the Caribbean also posted modest gains, supported by steady manufacturing output and sustained intra-regional trade flows. However, these increases were insufficient to offset the scale of contraction in Middle Eastern operations.

North America registered a slight decline, reflecting weaker transatlantic demand and normalisation following previously elevated trade volumes.

Route-Level Divergence Highlights Structural Shift

At the corridor level, performance diverged sharply depending on exposure to Gulf transit routes.

Europe–Asia emerged as the strongest long-haul trade lane, expanding 14.2% year-on-year, continuing a multi-year growth trajectory driven by manufacturing and technology shipments.

Intra-Asia trade also remained resilient, growing 7.5%, supported by regional production networks and sustained electronics and industrial demand.

By contrast, Middle East-linked corridors saw severe contraction. Asia–Middle East flows declined 58.6%, while Europe–Middle East routes fell 57.6%, reflecting the near-collapse of traditional transit-based cargo movement through Gulf hubs.

Freighter Networks Outperform Passenger Belly Capacity

Cargo type segmentation revealed a clear divergence in performance between dedicated freighter and passenger bellyhold capacity.

Dedicated freighter operations proved significantly more resilient, declining just 0.9% year-on-year as operators redirected capacity to alternative routes and maintained schedule stability through flexible network deployment.

In contrast, passenger belly cargo volumes fell 12.1%, driven by reduced flight frequencies, schedule adjustments, and network realignment by airlines responding to airspace restrictions and fuel cost pressures.

This divergence underscores the increasing structural importance of dedicated freighter fleets in maintaining global cargo continuity during periods of geopolitical disruption.

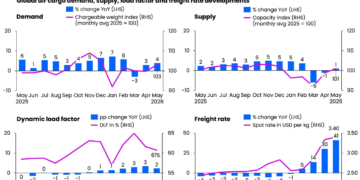

Capacity Tightness Mirrors Demand Contraction

Global available cargo tonne-kilometres (ACTK) declined 4.7% year-on-year, closely tracking the contraction in demand and reflecting widespread operational adjustments across airline networks.

Capacity reductions were most pronounced in the Middle East and parts of Africa, where operational constraints and rerouting limitations restricted utilisation.

Conversely, Asia Pacific, Europe, and Latin America recorded capacity increases driven by redeployment of aircraft and rerouting strategies. However, these gains were insufficient to compensate for the sharp reduction in Gulf-based connectivity.

Load Factors Stable Despite Regional Volatility

Despite falling demand and reduced capacity, the global cargo load factor remained stable at 47.9%.

This stability, however, masks significant regional divergence. Africa and Asia Pacific recorded stronger utilisation rates due to rerouted flows, while the Middle East experienced severe underutilisation following network disruption.

North America saw a gradual normalisation in load factors following elevated performance in the previous year.

Fuel Costs Intensify Inflationary Pressure

The market faced additional pressure from a sharp escalation in energy costs. Jet fuel prices rose 106.6% year-on-year, reaching their highest level in more than two decades, while Brent crude increased 43.1%.

These increases fed directly into airfreight pricing structures, amplifying yield pressures across long-haul trade lanes.

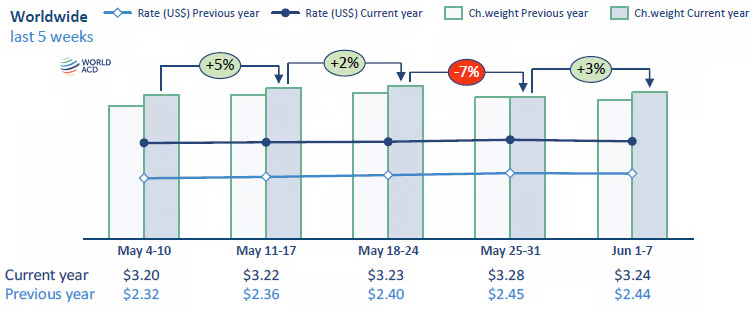

Average global air cargo rates rose 13.6% year-on-year to USD 2.75 per kilogram, driven by higher fuel surcharges, longer routing structures, and reduced maritime competitiveness in certain trade lanes.

Macroeconomic Conditions Remain Mildly Expansionary

Despite weakening momentum in freight volumes, broader macroeconomic indicators continued to signal modest expansion.

Global manufacturing output remained above the neutral threshold at 51.4, while new export orders stood at 50.1, indicating marginal growth in global trade activity.

Industrial production and global merchandise trade also expanded, although both showed signs of moderation, suggesting a cooling cycle rather than a structural downturn in demand.

Outlook: Structural Disruption Reshapes Global Air Cargo Network

The March 2026 air cargo environment reflects a convergence of cyclical softness and structural disruption, with geopolitical instability in the Middle East emerging as the defining factor reshaping global freight flows.

While rerouting strategies have supported resilience in certain regions, the loss of Gulf hub efficiency has fundamentally altered global connectivity patterns, increasing reliance on alternative corridors and freighter capacity.

As fuel volatility persists and network structures continue to adjust, the air cargo industry is entering a phase characterised by uneven regional performance, elevated cost structures, and a reconfiguration of traditional east–west trade routes.

{kind=link}