Global air cargo markets are experiencing a paradoxical trend: while freight volumes remain largely stagnant, airfreight rates continue to climb, driven primarily by record-high jet fuel prices rather than capacity constraints. Data from WorldACD covering the week of 23–29 March 2026 (week 13) shows a flat global cargo tonnage, even as pricing momentum pushed average full-market rates to a new annual peak of US$2.98 per kilogram.

Traffic Volumes Remain Flat

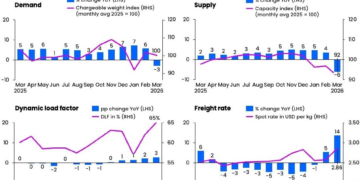

Worldwide chargeable weight remained unchanged from the previous week, reflecting a mixed regional performance. Four of the six major origin regions reported slight declines, while Asia Pacific (+2%) and Europe (+1%) registered modest weekly gains. Compared with the same period last year, global volumes were down 6%, with Central & South America (+7%) the only region showing year-on-year growth. The Middle East and South Asia (MESA) and Africa were the hardest hit, down 25% and 21% respectively.

The ongoing Middle East conflict continues to influence capacity and cargo flows. Airlines based in the Gulf have gradually rebuilt services, but passenger schedule constraints and geopolitical risks limit full recovery. On a two-week basis from 16–29 March, MESA-origin capacity increased +31% versus the previous fortnight, yet remained 33% below year-ago levels. Africa saw a +15% capacity uptick, supported by resumed Gulf airline services.

Price Momentum Driven by Jet Fuel

Spot rates continued their upward trajectory, reflecting surging jet fuel costs that have more than doubled since the outbreak of the Iran war in late February. Week-on-week, average global air cargo rates increased +5%, moderating from a +10% gain in week 11.

MESA-origin routes illustrate the divergence between volumes and pricing. Traffic from Dubai to Europe fell -3% week-on-week, down -31% year-on-year, yet rates surged +28% WoW, reaching $5.44/kg—triple the rate from the same period in 2025. Rates from Colombo climbed to $4.77/kg (+2x YoY). MESA-origin shipments to the US saw a +9% weekly increase, with Dubai at $10.33/kg, up 152% from last year. Other origins such as India registered single-digit rate gains, yet still stood +70% above 2025 levels at $7.77/kg.

Asia Pacific Airfreight Trends

Asia Pacific-origin shipments showed minimal week-on-week volume growth: flat to the US and +1% to Europe. Spot rates, however, continued to rise, reinforcing the fuel-cost-driven pricing environment. Rates from Asia Pacific to the US increased +9% WoW, reaching $5.91/kg, led by China and South Korea (+13% WoW). To Europe, rates rose +4% WoW, representing a +28% increase YoY, with Indonesia recording a dramatic +41% weekly surge and +115% YoY. Singapore (+95% YoY) and Taiwan (+9% WoW) also contributed to upward pressure.

Regional volume anomalies were largely attributed to the Eid-al-Fitr holiday, which reduced shipments from Indonesia (-45% to US, -27% to Europe) and Malaysia (-11% to US, -14% to Europe).

Outlook

With northern hemisphere carriers transitioning to summer schedules in early April, seasonal capacity adjustments are expected. Nevertheless, the prevailing factor shaping rates remains elevated jet fuel costs, exacerbated by geopolitical instability in the Middle East. Market observers anticipate that fuel prices, rather than underlying demand or capacity constraints, will continue to dictate rate momentum in the near term.

Airlines and shippers alike are navigating this complex environment, balancing cost pressures with the need to maintain supply chain reliability amid ongoing regional disruptions.

{kind=link}