Global air cargo pricing appears to be entering a stabilisation phase following a sharp escalation in rates triggered by geopolitical disruption in the Middle East, according to the latest market analysis from freight data platform Xeneta.

The data suggests that while April 2026 marked one of the most significant year-on-year spikes in airfreight pricing in recent periods, underlying market fundamentals are beginning to reassert themselves as capacity gradually returns across key trade lanes.

Sharp April Surge Driven by Conflict and Capacity Tightening

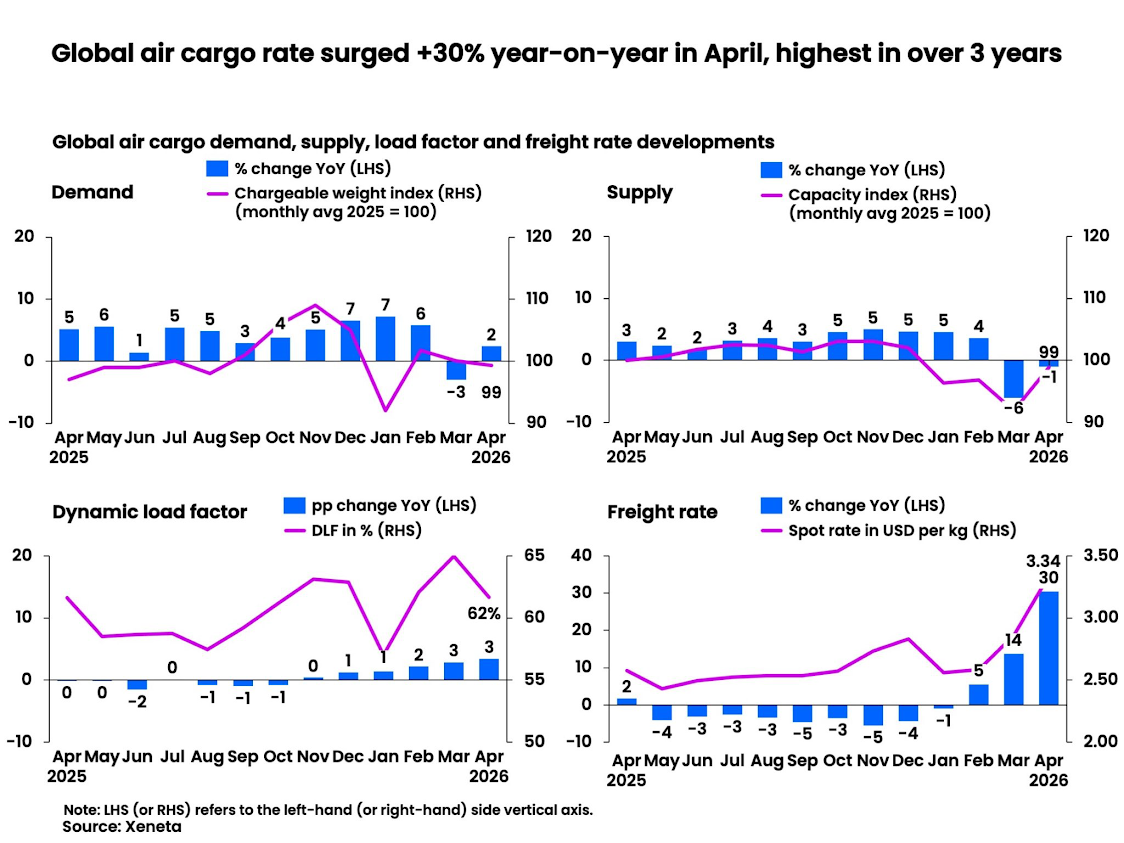

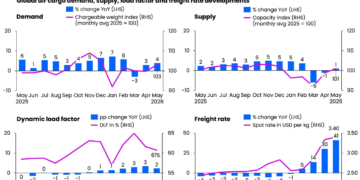

Xeneta’s monthly figures show that average global airfreight spot rates rose by more than 30% year-on-year in April to $3.34 per kilogram, reflecting a temporary but intense market disruption caused by escalating tensions in the Middle East.

The conflict contributed to higher jet fuel prices, rerouting of flight paths, longer transit times, and reduced effective capacity across multiple corridors. At the same time, global demand for air cargo increased by 2% year-on-year, while capacity contracted by 1%, pushing the dynamic cargo load factor up by three percentage points to 62%.

The combination of tighter capacity and elevated operating costs created a rapid upward repricing environment, particularly on Asia-origin trade lanes.

Market Correction Underway as Capacity Returns

However, analysts at Xeneta indicate that the market may now be transitioning out of its peak pricing phase as capacity begins to recover in previously disrupted regions.

According to chief airfreight officer Niall van de Wouw, the rapid rate escalation observed in April is unlikely to be sustained at the same pace moving forward.

“Now capacity is coming back, rates will come down, but not as quickly as they went up. Ultimately, market fundamentals will prevail,” he said.

Van de Wouw emphasised that while fuel prices played a role in recent volatility, airfreight pricing is still predominantly driven by the balance between supply and demand rather than fuel surcharges alone.

He noted that recent developments in transatlantic pricing illustrate this disconnect, with rates declining in recent weeks despite rising jet fuel costs.

Fuel Costs Less Influential Than Market Structure

The data also suggests that fuel surcharges are not the primary driver of current rate dynamics, despite widespread cost pressures across the aviation sector.

“The all-in cost a freight forwarder pays an airline is more driven by demand and supply than it is by fuel costs,” van de Wouw explained, adding that many surcharge mechanisms remain negotiable and inconsistently applied across markets.

He also suggested that airline responses to fuel volatility are unlikely to significantly disrupt cargo capacity in the long haul segment, where most international freight is carried.

Long-haul routes, which account for the majority of global air cargo volumes, are expected to remain relatively stable compared to domestic and regional passenger services that may be more vulnerable to schedule adjustments.

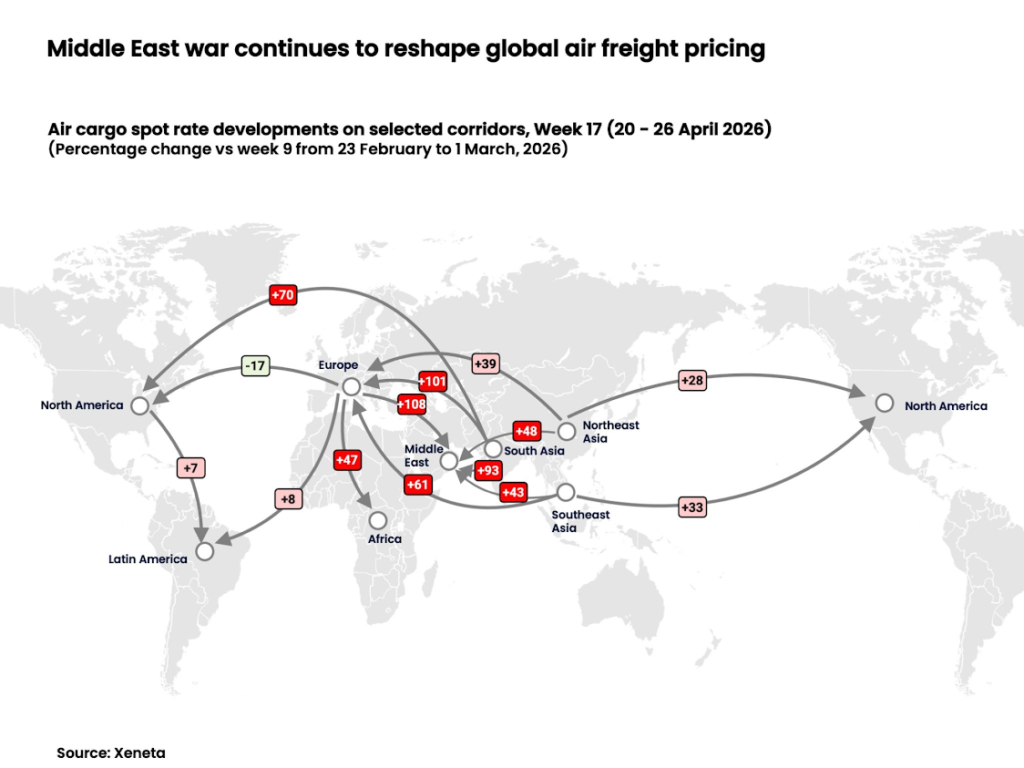

Regional Rate Divergence Across Asia

Xeneta’s analysis highlights significant variation in pricing trends across Asian export markets, reflecting differing levels of exposure to fuel impacts and capacity constraints.

In South Asia, airfreight rates appear to have peaked in mid-April, followed by a modest single-digit decline toward the end of the month as market pressure eased.

Southeast Asia saw sharper increases earlier in the month, with spot rates to the Middle East and Europe rising by 43% and 61% respectively compared to pre-conflict levels, reaching $3.78 and $5.12 per kilogram. Rates to North America increased by 33% to $6.46 per kilogram.

Despite these gains, Xeneta notes that pricing on Europe and North America-bound routes is now showing early signs of stabilisation, while Middle East lanes remain more volatile.

Northeast Asia Lags with Delayed Pricing Response

Northeast Asia exhibited a slower but steady upward adjustment, with outbound rates to the Middle East, Europe, and North America reaching $5.25, $5.63, and $5.54 per kilogram respectively in the final week of April.

However, percentage increases in the region were more moderate compared to South and Southeast Asia, a divergence attributed to delayed fuel surcharge adjustments rather than immediate market fundamentals.

Xeneta noted that jet fuel price peaks in early April had not yet been fully passed through to all market participants, resulting in lagged pricing responses across certain trade lanes.

Europe–North America Corridor Sees Rate Decline

In contrast to Asia-origin volatility, the Europe–North America corridor experienced downward pressure on rates, with prices falling 17% compared to pre-conflict levels to $2.57 per kilogram.

This decline occurred despite higher fuel costs, as increased passenger flight schedules for the summer season injected additional bellyhold capacity into the market.

Cargo load factors on the route fell by ten percentage points month-on-month, leading to oversupply conditions and downward pricing pressure.

Demand Outlook and Structural Concerns

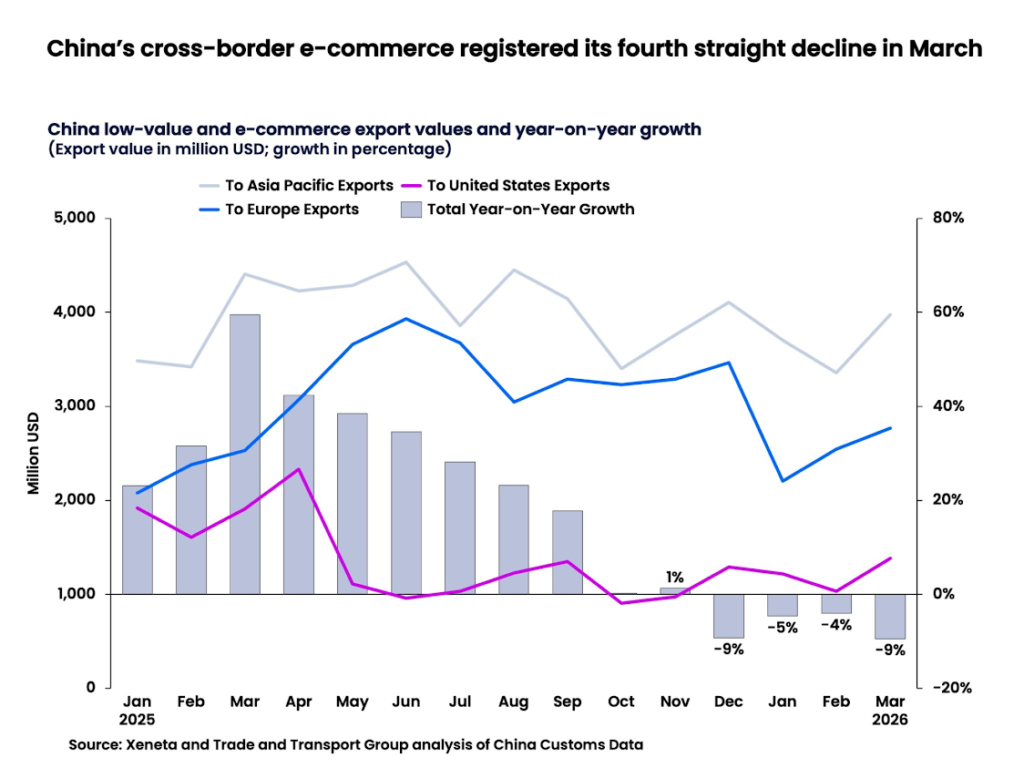

Looking ahead, Xeneta warns that broader macroeconomic conditions may continue to weigh on airfreight demand, particularly in the e-commerce segment.

Data shows a 9% year-on-year decline in e-commerce volumes out of China in March, although some of this reduction may reflect shifting flows into consolidated airfreight channels not fully captured in origin-based statistics.

Van de Wouw suggested that while some rebalancing is occurring, the underlying trajectory points to a slowdown in traditional B2C-driven growth.

“The B2C e-commerce growth seems to be over,” he said, pointing to a consistent downward trend in non-China-origin volumes over the past four months.

Peak Pricing Likely Passed, but Volatility Remains

Despite easing conditions in several key markets, Xeneta cautions that uncertainty remains a defining feature of the 2026 air cargo outlook, particularly given ongoing geopolitical risks and structural shifts in global trade flows.

“The peak for global airfreight rates is likely behind us,” van de Wouw concluded, “but there will undoubtedly be continued concern about what comes next in terms of trade disruption.”

While the immediate pricing shock appears to be stabilising, the market is entering a phase characterised by uneven recovery, regional divergence, and persistent sensitivity to external shocks—suggesting that volatility, rather than stability, may define the next cycle of airfreight performance.

{kind=link}