Global air cargo spot rates continued their upward trajectory in May 2026, reaching their highest levels in more than three years, although emerging market indicators suggest that pricing momentum may begin to ease in the coming months as capacity recovers and demand growth moderates.

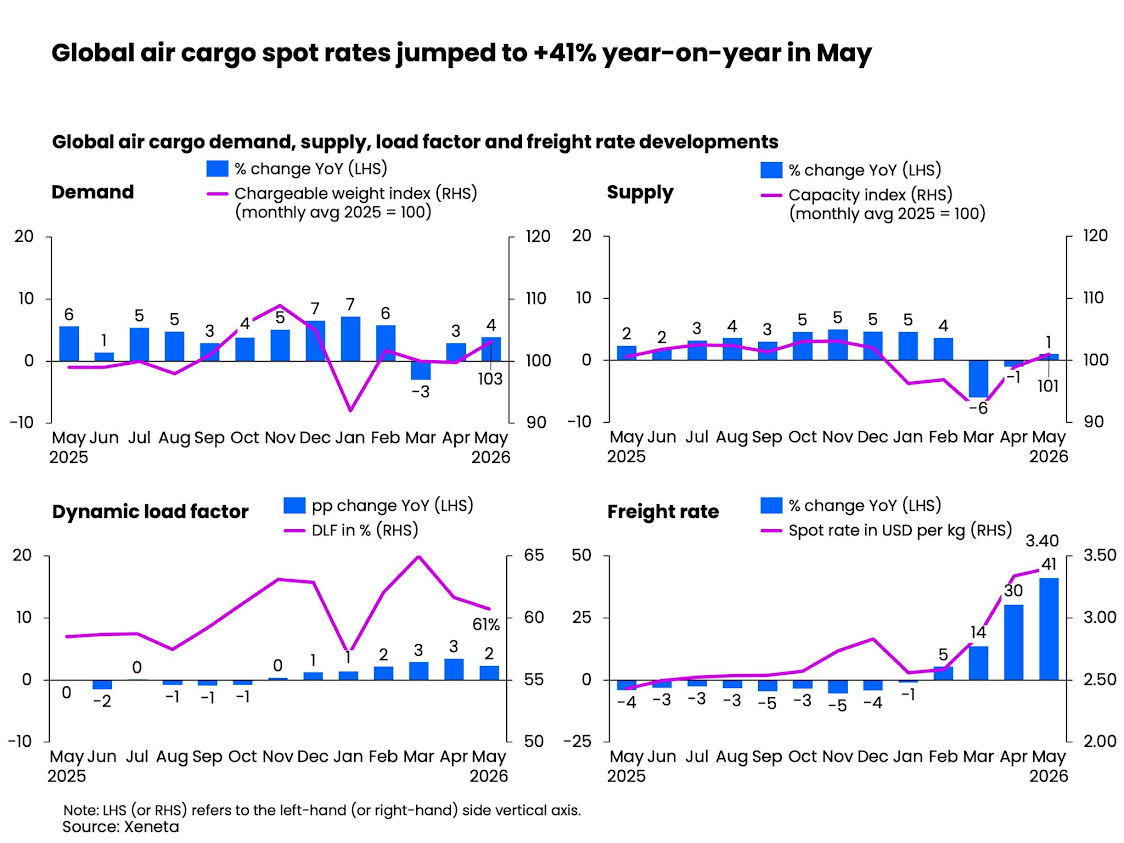

According to the latest market analysis from Xeneta, average global air cargo spot rates increased by 41% year-on-year during May, reaching US$3.40 per kilogram. The rise follows strong market performance in April and reflects a supply-demand imbalance that has continued to favor carriers despite ongoing uncertainty across global trade and logistics markets.

However, while demand remained resilient throughout May, industry analysts are increasingly pointing to signs that the market may have reached its pricing peak, with long-term contract rates already showing signs of stabilization and downward adjustment.

Demand Continues to Outpace Capacity

The primary driver behind elevated freight rates remains the strength of global air cargo demand relative to available capacity.

Xeneta reported that worldwide air cargo demand increased by 4% year-on-year during May, while dynamic load factor—a key indicator of capacity utilization based on cargo volumes, weight carried, and available capacity—rose by two percentage points to 61%.

The increase highlights continued pressure on available cargo space, despite gradual improvements in airline capacity deployment.

Throughout the first half of the year, global air freight markets have been influenced by geopolitical tensions, particularly disruptions linked to conflict in the Middle East. These challenges temporarily constrained capacity across several key trade corridors and contributed to higher freight rates worldwide.

However, airline capacity has steadily recovered and finished May approximately 1% above levels recorded during the same period last year.

With Middle Eastern carriers progressively restoring operations and reintroducing capacity to the market, analysts expect additional supply to place downward pressure on freight rates during the coming weeks.

Xeneta Predicts Softer Market Conditions

Niall van de Wouw, Chief Airfreight Officer at Xeneta, believes the market is entering a transitional phase where pricing will gradually adjust to improving capacity conditions.

While rates are unlikely to fall as rapidly as they climbed earlier this year, he indicated that year-on-year spot rate comparisons could begin turning negative as early as June.

According to Xeneta, several key industry sectors are currently experiencing slower growth, reducing the likelihood of another major surge in air cargo demand during the traditionally quieter summer period.

The Northern Hemisphere summer season typically sees significant passenger capacity returning to the market, adding additional bellyhold cargo space and contributing to softer freight pricing.

Although rate declines often lag changes in market fundamentals, analysts increasingly view the summer months as a period of normalization following the extraordinary volatility experienced during the first half of 2026.

Long-Term Rates Signal Market Peak

One of the clearest indicators of changing market sentiment is the behavior of long-term freight rates.

While contract rates remained 22% higher than a year earlier, Xeneta noted that these rates began easing after reaching a peak in late April.

This development suggests that shippers, freight forwarders, and airlines increasingly believe current pricing levels represent the high point of the cycle.

Long-term contracts are often viewed as a leading indicator of future market direction because they reflect expectations regarding future supply-demand conditions.

The recent moderation therefore points toward a more balanced market environment in the second half of the year.

Artificial Intelligence Drives Transpacific Demand

Despite expectations of a broader market slowdown, several trade corridors continue to experience strong demand supported by specific industry sectors.

Among them, artificial intelligence infrastructure development has emerged as one of the most significant demand drivers in global air cargo.

Shipments related to semiconductors, advanced computing hardware, servers, and data centre infrastructure continue to generate strong volumes on Transpacific routes, making the corridor one of the strongest-performing air freight markets in 2026.

The rapid expansion of AI-related investments worldwide has created sustained demand for high-value, time-sensitive cargo transportation, benefiting carriers operating between Asia and North America.

Middle East Disruptions Continue to Influence Rates

Geopolitical instability also remains an important factor affecting air freight pricing.

Renewed missile activity and ongoing security concerns during periods of attempted ceasefire in the Middle East disrupted the recovery of cargo capacity in several regional markets during May.

As a result, freight rates on routes connecting Europe, South Asia and Southeast Asia with Middle Eastern destinations remained significantly elevated.

Some spot rates increased by as much as 113% compared with levels recorded in late February, highlighting the continuing impact of regional instability on global cargo networks.

Although rates have retreated from their April highs, they remain well above historical averages on several affected corridors.

Europe-North America Market Faces Different Dynamics

In contrast, the Europe-to-North America market has exhibited a different trend.

While transatlantic cargo demand strengthened during May, airlines have introduced substantial additional capacity through expanded summer passenger schedules.

The resulting increase in available bellyhold cargo space has exerted downward pressure on freight rates, making the corridor one of the few major trade lanes where pricing remains below year-earlier levels.

The situation illustrates how capacity availability continues to play a decisive role in determining freight rate performance across different markets.

E-Commerce Growth Slows but Remains Significant

One of the most notable developments in the air cargo market has been the gradual slowdown in cross-border e-commerce growth.

China’s low-value and e-commerce exports declined by 11% year-on-year in April, marking the fifth consecutive month of contraction.

The decline has been particularly pronounced on shipments destined for the United States, where volumes fell by 33%.

European-bound e-commerce shipments declined by 6%, while Asia-Pacific volumes decreased by only 1%.

Industry experts caution, however, that these figures do not necessarily indicate a collapse in e-commerce demand.

Instead, a growing proportion of shipments are being consolidated into larger bulk freight movements that fall outside traditional parcel-tracking statistics.

This shift reflects evolving logistics strategies rather than a fundamental reduction in consumer demand.

Regulatory Changes Could Reshape E-Commerce Flows

The regulatory environment is also becoming more challenging for international e-commerce operators.

Beginning 1 July, the European Union will abolish its €150 de minimis exemption and introduce a flat €3 duty on individual items imported from outside the bloc.

An additional €2 handling fee is expected to be implemented later in the year.

The measures are primarily aimed at managing the rapid growth of low-value shipments from major online retail platforms and could significantly alter shipping patterns across Europe.

Previous examples suggest that sudden regulatory changes can lead to rerouting of cargo volumes between neighboring countries as logistics providers adapt their networks to minimize costs and disruptions.

Despite these challenges, Xeneta expects e-commerce platforms to adjust quickly, as they have done following previous regulatory changes in major markets.

Tariff Uncertainty Adds Further Complexity

Beyond e-commerce regulation, the air cargo sector is also monitoring evolving trade policy developments.

In early June, the United States Trade Representative proposed additional tariffs ranging from 10% to 12.5% on imports from approximately 60 trading partners, including China and the European Union.

The proposal is linked to concerns regarding enforcement of restrictions on goods associated with forced labor and remains subject to public hearings and review.

Should the tariffs be implemented, they could influence manufacturing decisions, sourcing strategies, and transportation demand patterns across multiple industries.

Ocean Freight Trends May Influence Air Cargo Demand

Another factor being closely watched by the industry is the growing trend of cargo frontloading in ocean freight markets.

Many shippers are accelerating production and transportation schedules in anticipation of potential increases in energy costs, future tariff measures, and traditional peak-season freight surcharges.

This activity has already contributed to stronger demand and higher rates in maritime logistics.

According to Xeneta, prolonged frontloading activity could eventually spill over into the air cargo sector if companies seek faster transportation options to support inventory strategies.

Market Outlook: Cautious Optimism Amid Cooling Demand

While global air cargo markets remain fundamentally healthy, the outlook for the second half of 2026 appears more balanced than the exceptionally strong conditions seen earlier this year.

Demand continues to exceed capacity in several important sectors, particularly technology and specialized cargo segments, but improving airline capacity and slower growth in e-commerce and manufacturing are expected to moderate pricing.

Industry observers anticipate that air freight rates will remain above historical averages, though the extraordinary growth recorded during the first half of the year is unlikely to be sustained.

As airlines restore capacity, geopolitical risks evolve, and global trade policies continue to shift, the market appears to be entering a phase characterized by greater stability and more moderate rate growth.

{kind=link}