The global air cargo market continued its strong performance through June 2026, with worldwide chargeable weight increasing 9% year-on-year, underscoring the sector’s resilience despite geopolitical tensions, shifting trade regulations and ongoing capacity adjustments.

According to the latest WorldACD Market Data weekly market analysis, June volumes remained broadly stable compared with May, while average freight rates stayed significantly above last year’s levels, although both tonnage and pricing eased slightly during the final full week of the month. The figures cover the five-week period ending 28 June 2026 and reflect a market that continues to benefit from robust international demand despite recent disruptions. The reported data aligns with the latest market updates published by WorldACD Market Data and fuel pricing information released through IATA’s Jet Fuel Price Monitor.

First-half volumes post solid growth

The first six months of 2026 delivered encouraging results for the air cargo industry, with global chargeable weight rising 5% year-on-year.

Second-quarter (Q2) volumes were 6% higher than the same period in 2025 and also 6% above the first quarter, highlighting sustained momentum across major trade lanes.

The strongest contribution came from the Asia-Pacific region, where outbound cargo volumes increased 8% during the first half of the year, reaffirming the region’s position as the world’s principal air cargo production hub.

Despite ongoing operational challenges caused by instability in the Middle East and temporary capacity disruptions, international cargo demand remained resilient across most major markets.

Middle East and Asia-Pacific lead June growth

Regional performance during June reflected broad-based expansion across most key export markets.

The strongest year-on-year increase originated from Middle East & South Asia (MESA), where tonnage climbed 11%, supported in part by the calendar shift of Eid al-Adha, which fell in May this year compared with June in 2025.

The Asia-Pacific region followed closely with 10% growth, while North America recorded a 9% increase.

European exports expanded 7%, matching the growth achieved by Central and South America, whereas Africa experienced comparatively modest growth of 1%.

The widespread gains indicate that global trade flows continue to normalise despite geopolitical uncertainty and evolving customs regulations.

Air cargo rates remain historically elevated

Although weekly market activity softened toward the end of June, freight pricing remained considerably stronger than a year ago.

Average worldwide air cargo rates during June were approximately 33% higher year-on-year, maintaining the elevated pricing environment that has characterised much of 2026.

Average rates for the second quarter also stood 28% above first-quarter levels, illustrating the significant market shift following the geopolitical tensions that escalated in the Middle East earlier this year.

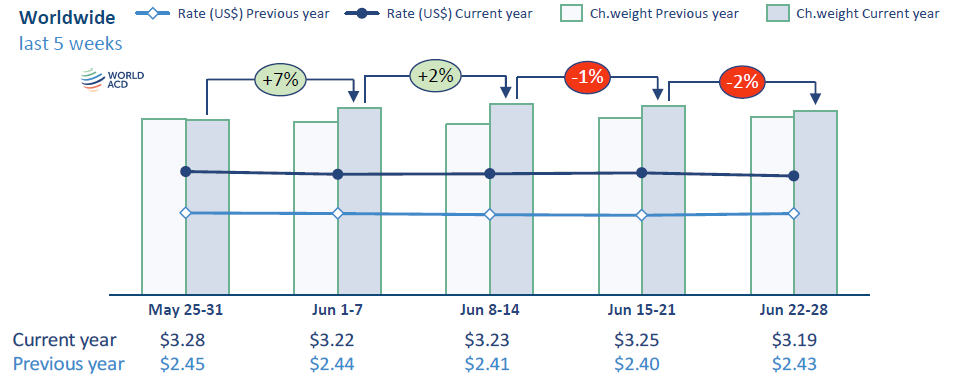

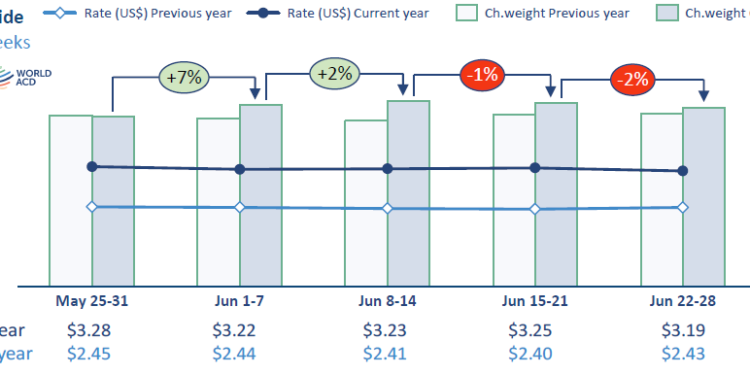

Worldwide spot rates averaged US$3.71 per kilogram during June, remaining largely unchanged from May.

Compared with June 2025, however, spot prices were still 43% higher, although this represented a moderation from the 49% annual increase recorded in May.

Regional spot rate performance remained particularly strong:

- Middle East & Africa: +49%

- Asia-Pacific: +47%

- North America: +42%

- Europe: +34%

- Central & South America: +14%

These figures demonstrate that pricing continues to reflect constrained supply-demand dynamics across several major trade corridors, even as capacity steadily returns to the market.

Falling fuel prices begin easing cost pressures

One factor likely to influence freight pricing during the coming months is the continued decline in aviation fuel costs.

According to IATA’s Jet Fuel Price Monitor, jet fuel prices fell by a further 2% week-on-week during the week ending 26 June, dropping below US$117 per barrel, while Brent crude oil declined 9% to below US$74 per barrel.

The reduction follows a period of relative stability after recent diplomatic developments between the United States and Iran eased immediate concerns surrounding energy markets.

Several airlines have already announced reductions in fuel surcharges effective from 1 July, suggesting that overall air freight rates could soften further if lower fuel prices persist.

Capacity recovery gathers momentum

The gradual stabilisation of Middle Eastern operations has also supported continued improvements in global cargo capacity.

Comparing the most recent two-week period with the previous fortnight, worldwide available cargo capacity increased 3%.

The strongest recovery was recorded in Middle East & South Asia, where capacity expanded 5%, followed by North America (4%) and Europe (3%).

Overall global capacity is now 3% higher than the same period last year, with Middle Eastern capacity also returning slightly above 2025 levels.

The improved availability is expected to enhance schedule reliability while contributing to greater pricing stability across international markets.

New EU customs rules have limited market impact

Unlike the significant shipment acceleration witnessed ahead of previous United States import policy changes, the introduction of the European Union’s revised de minimis customs rules on 1 July generated little evidence of widespread front-loading.

Under the new regulation, imports into the EU valued below €150 are now subject to a €3 fixed customs handling fee per shipment or tariff code.

Despite expectations that exporters might accelerate shipments before implementation, cargo demand from Asia weakened during the final week of June.

Volumes from China to Europe declined 8% week-on-week, while shipments from Hong Kong dropped 9%.

Other major export markets also recorded lower weekly demand, with cargo from Vietnam decreasing 7% and Thailand falling 9%, resulting in an average 7% decline in Asia-Pacific exports to Europe.

Industry observers suggest that the muted market response reflects lessons learned from previous changes to United States de minimis regulations, with more efficient and lower-cost customs declaration systems now helping exporters minimise compliance costs.

Even with the softer demand, average spot rates from Asia-Pacific to Europe remained resilient at US$5.26 per kilogram, only 2% lower week-on-week while still standing 38% above last year’s level.

Market outlook remains positive

While weekly volumes eased slightly at the end of June, the broader picture remains positive for the global air cargo industry.

Robust year-on-year demand, improving capacity, easing fuel costs and resilient international trade continue to support healthy market fundamentals.

Although freight rates may moderate as additional capacity returns and lower fuel surcharges take effect, the first-half performance demonstrates that the industry has successfully navigated geopolitical disruption and regulatory change while maintaining strong growth across most major cargo regions.

{kind=link}