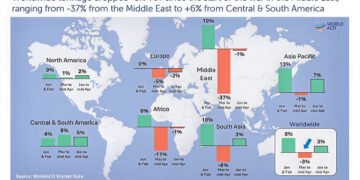

Global air cargo markets entered the second quarter of 2026 under mounting operational and commercial pressure as continuing geopolitical instability across the Middle East disrupted established routing patterns, tightened effective capacity, and pushed freight rates higher across major international corridors.New market intelligence from DHL Global Forwarding indicates that airfreight markets remain in a supply-constrained phase, with airlines facing persistent network disruptions, elevated jet fuel costs, and reduced schedule reliability as carriers continue rerouting flights around restricted Gulf airspace.According to DHL’s April 2026 Air Freight Market Update, global air cargo demand declined 4 percent year on year in March 2026, while available cargo capacity was down 3 percent year on year as of late April, reflecting the sharpest contraction in the Gulf region since the crisis began. At the same time, spot rates remained structurally elevated, rising 45 percent year on year during week 17 as supply shortages intensified. Industry analysts say the disruption is no longer regional. What began as an operational challenge centered on Gulf hub connectivity has now evolved into a global network issue, affecting cargo flows between Asia, Europe, Africa, and the Americas.

Gulf Airspace Restrictions Reshape Global Networks

Airspace closures and military restrictions across parts of the Middle East continue to force carriers to bypass traditional transit hubs, extending flight times, increasing fuel burn, and reducing aircraft utilization.DHL said the ongoing crisis is “reshaping networks,” with rerouting continuing to suppress export activity from Gulf hubs while reducing schedule reliability across Europe-, Africa-, and Asia-linked trade lanes. The most significant impact has been felt across Middle East and Africa, where export volumes fell 24 percent year on year in March, making it the weakest-performing origin region globally.With major Gulf carriers still operating below pre-crisis levels, capacity restoration remains incomplete despite gradual recovery in freighter operations. DHL noted that airlines including Emirates, Etihad, and Qatar Airways have progressively reintroduced services, but capacity remains constrained and rates continue to sit above historical averages.

Europe Absorbs Secondary Shock

Europe’s air cargo sector has also felt the downstream effects of the Gulf disruption.March cargo demand from Europe declined 5 percent year on year, underperforming the global average as airlines shifted capacity toward direct long-haul services and alternative hub strategies to reduce dependence on Middle East transit points.While these adjustments have preserved network continuity, they have also introduced higher operating costs, particularly as jet fuel prices remain elevated amid ongoing energy market volatility.

Asia Pacific Shows Mixed Performance

In Asia Pacific, overall air cargo demand declined 4 percent year on year, although intra-Asia trade remained resilient, growing 7 percent on the back of continued demand for semiconductors, AI-related components, consumer electronics, and high-value technology shipments.DHL noted that intra-regional demand continues to anchor Asian cargo performance even as long-haul corridors face tighter capacity and rising surcharges.Asia-Europe lanes have been particularly affected by Middle East rerouting requirements, with carriers applying emergency fuel and operational surcharges as block times increase and aircraft rotations become less efficient.

Latin America Emerges as Growth Outlier

While most major regions reported declining demand, Latin America posted 9 percent year-on-year export growth, supported by stronger Asia-bound perishables and agricultural shipments.However, the seasonal strength in perishables has also created additional pressure on available uplift, displacing general cargo and tightening space on key long-haul services.

North America Holds Steady

North American cargo demand remained broadly flat during March, with rerouted international flows helping offset disruption elsewhere.Analysts noted that transpacific and transatlantic corridors have remained relatively stable compared with Middle East-linked networks, although pricing continues to reflect broader global supply constraints.

Fuel Costs Add Further Pressure

Beyond geopolitical risk, airlines are also facing persistently high jet fuel prices, further increasing operating expenses.DHL said carriers have responded through route suspensions, aircraft redeployment, and emergency surcharges across multiple trade lanes, with fuel-related cost recovery becoming an increasingly important pricing mechanism. The pressure is not isolated to cargo operators. Redington confirmed this week that it has shifted more shipments to airfreight despite rising costs, rerouting products via Saudi Arabia and Oman to maintain supply into Gulf markets amid continued disruption.

Outlook: Volatility to Continue Through Q2

Despite the operational disruption, DHL continues to forecast 2 to 3 percent full-year air cargo demand growth for 2026, supported by structural demand from semiconductor manufacturing, artificial intelligence infrastructure, pharmaceutical shipments, and high-value electronics.However, the company warned that effective capacity is likely to remain tight throughout the second quarter as geopolitical uncertainty, fuel volatility, and aircraft redeployment continue to constrain supply.With cargo networks increasingly being redesigned around resilience rather than efficiency, industry observers say the Gulf crisis may leave a lasting structural impact on how global airfreight capacity is allocated well beyond 2026.

{kind=link}