The closure of Middle Eastern airspace has triggered a sharp contraction in global air cargo capacity, with fresh data indicating an immediate and measurable impact on worldwide freight flows.

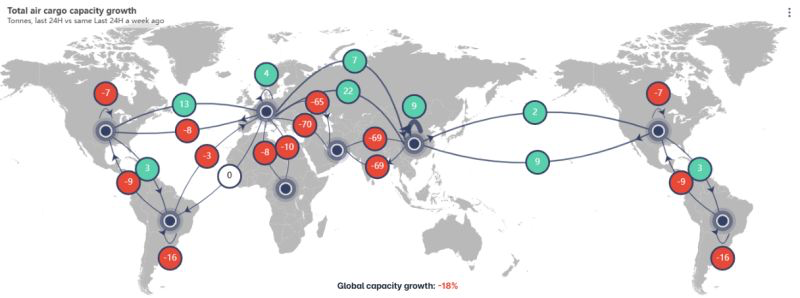

According to Rotate’s Live Capacity data, approximately 13 percent of global air cargo lift is directly affected by the restrictions. Within just 24 hours of the first major flight suspensions, total global capacity fell by 18 percent compared with the same period the previous week — a significant shock to an industry already navigating geopolitical volatility and fragile trade flows.

The disruption follows escalating tensions linked to US and Israeli strikes on Iran, which have resulted in widespread airspace closures and airport shutdowns across parts of the region.

Gulf Carriers Grounded

At the centre of the capacity contraction is the temporary suspension of services by leading Gulf carriers, including Qatar Airways, Emirates and Etihad Airways. Collectively, these airlines represent a substantial share of long-haul bellyhold and freighter capacity connecting Asia, Europe and Africa.

Tim van Leeuwen, Vice President and Head of Consulting at Rotate, said the figures underscore the structural importance of Middle Eastern hubs within global supply chains.

“As the scale and impact of the US/Israel strikes on Iran becomes more clear, it is already evident that Middle East airspace closures will have a significant effect on the air cargo industry, with Rotate Live Capacity data showing 13 percent of global air cargo capacity directly affected,” he noted.

Van Leeuwen highlighted the magnitude of the interruption. Prior to the suspensions, Qatar Airways was operating approximately 12,000 tonnes of daily cargo capacity, while Emirates accounted for around 10,000 tonnes per day. The temporary withdrawal of this lift has immediate consequences for time-sensitive supply chains and intercontinental trade lanes.

Having initially reported that around 12 percent of global capacity would be impacted, Rotate’s updated figures now show an 18 percent global decline within a 24-hour window compared with last week.

Three Drivers Behind the Capacity Drop

Rotate identifies three principal factors behind the sudden contraction:

- Middle Eastern carriers suspending operations, at least temporarily

- Non-regional airlines halting services to Gulf destinations without short-term alternatives

- Freighter aircraft rerouting to alternative technical stops or operating longer direct sectors, affecting payload and network balance

The Middle East’s role as a strategic bridge between East and West means that even partial closures reverberate across multiple trade corridors. Asia–Europe flows, in particular, are facing structural adjustments as airlines redesign routings to bypass restricted airspace.

Counterintuitive Shifts in Asia–Europe Flows

Interestingly, Rotate’s data reveals that Asia–Europe capacity increased by 22 percent during the same period. This rise is attributed to carriers switching technical stops to Central Asian airports or operating direct long-haul sectors rather than routing via Gulf hubs.

However, analysts caution that this increase does not offset the broader systemic disruption. Longer routings can reduce payload due to weight restrictions, increase fuel burn, and disrupt finely balanced hub-and-spoke networks. Moreover, the temporary capacity boost on specific corridors may prove unsustainable if airspace restrictions persist.

Network Reshaping Underway

The suspension of Gulf carrier operations is not merely a short-term scheduling issue; it is reshaping global airfreight networks in real time. The Middle East has long functioned as a central transhipment crossroads for intercontinental cargo. With that bridge partially removed, airlines are being forced to adopt more fragmented, point-to-point solutions.

The coming days will determine whether capacity stabilises through alternative routings or whether prolonged closures lead to sustained rate volatility and supply chain bottlenecks.

For now, the data confirms what many forwarders and shippers are already experiencing: a rapid and significant tightening of global air cargo lift capacity driven by geopolitical escalation in one of aviation’s most strategically vital regions.

{kind=link}