Global air cargo demand continued its upward trajectory in June 2026 as surging shipments of semiconductors and artificial intelligence (AI) hardware offset a prolonged slowdown in cross-border e-commerce, according to the latest market analysis from Xeneta.

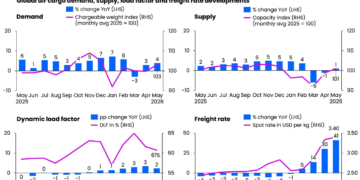

The industry intelligence provider reported that worldwide air cargo demand increased 7% year-on-year in June, while the pace of spot rate growth moderated as capacity returned to the Middle East, fuel prices eased and market conditions became more balanced. Despite softer pricing momentum, demand continued to outpace available capacity, highlighting the resilience of the global air freight market.

AI cargo replaces e-commerce as the market’s growth engine

Xeneta said the rapid expansion of AI infrastructure has become the principal driver of air cargo demand, replacing e-commerce, which had fuelled much of the industry’s growth over the past two to three years.

The increase in shipments of advanced semiconductors, AI processors and related high-value electronics has strengthened cargo flows, particularly on transpacific trade lanes linking Asia with North America.

Niall van de Wouw, Chief Airfreight Officer at Xeneta, described June’s performance as “remarkable,” noting that AI-related shipments are currently underpinning global air freight demand.

Although AI cargo accounts for less than 10% of total global air freight volumes, it is now contributing disproportionately to market growth.

The trend reflects exceptional demand across the semiconductor industry. Global semiconductor sales more than doubled in April, increasing 106% year-on-year—the strongest annual growth since records began in 1986. The surge has reinforced the Asia-Pacific–North America corridor as the strongest-performing air freight market of 2026, despite softer cargo volumes between China and the United States following tariff measures.

Asia’s semiconductor industry powers freight demand

Broader economic indicators also point to the growing influence of the AI supply chain on international logistics.

Taiwan, home to many of the world’s leading advanced semiconductor manufacturers, recorded 15% real GDP growthduring the first quarter of 2026—its fastest quarterly expansion in almost five decades.

Meanwhile, South Korea’s two largest semiconductor manufacturers have seen their market capitalisations more than double and triple respectively this year, together representing more than half the total value of the Seoul stock exchange.

These developments continue to generate sustained demand for time-sensitive air freight services transporting chips, servers, networking equipment and AI infrastructure across global markets.

Spot rate growth slows as market stabilises

While demand remained strong, pricing trends indicated a gradual return to more stable market conditions.

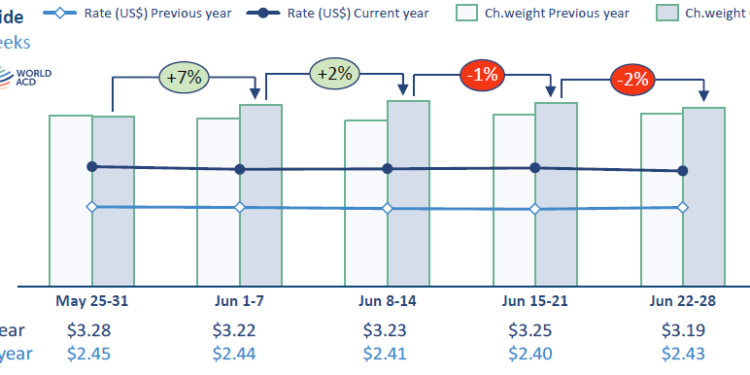

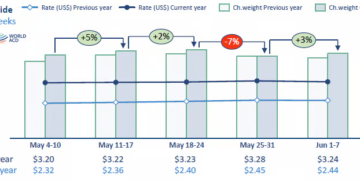

Global air cargo spot rates, applicable to shipments booked for up to one month, averaged US$3.40 per kilogram in June, representing a 38% year-on-year increase.

However, this marked a slight moderation from the 41% annual increase recorded in May.

Xeneta attributed the easing primarily to the reduction in geopolitical tensions in the Middle East, the restoration of capacity through major Gulf hubs and declining jet fuel prices.

Van de Wouw noted that the recent conflict involving the United States and Iran had driven freight rates substantially higher than anticipated earlier in the year, but pricing is now beginning to soften as market conditions normalise.

Even so, rates remain elevated on several AI-driven trade lanes.

During the final week of June, freight rates from Northeast Asia to North America were 41% higher than in late February, while rates from Southeast Asia to North America increased 42% over the same period.

Routes serving the Middle East also continued to command premium pricing despite signs of easing. Compared with pre-conflict levels, rates remained significantly higher from South Asia (+88%), Southeast Asia (+46%) and Europe (+79%), although additional capacity has begun placing downward pressure on prices.

Capacity growth trails demand

Global demand continued to outstrip supply throughout June.

Xeneta reported that worldwide air cargo demand increased 7%, while available capacity expanded by only 3%, largely due to the gradual return of services previously affected by Middle East disruptions.

As a result, Xeneta’s dynamic load factor—which measures the relationship between cargo demand and available capacity—rose by three percentage points year-on-year to 62%, indicating continued healthy aircraft utilisation across the market.

According to Xeneta’s latest Air Freight Outlook Update, global air cargo demand during the first half of 2026 increased 4% year-on-year, exceeding earlier expectations for a relatively subdued year.

Transatlantic market softens with passenger capacity

Not all trade lanes experienced upward pricing pressure.

The introduction of summer passenger schedules significantly increased belly-hold cargo capacity across the North Atlantic, contributing to a 25% decline in freight rates from Europe to North America compared with winter schedule levels in late February.

The trend illustrates how regional supply dynamics continue to influence pricing independently of global demand.

Xeneta also observed that freight pricing is increasingly being determined by capacity availability rather than fuel costs.

During the recent Middle East conflict, jet fuel prices rose sharply, yet transatlantic freight rates continued to decline due to increased capacity.

The company therefore recommends that air freight pricing mechanisms be based primarily on actual airline freight rates rather than fluctuations in fuel prices.

E-commerce continues to lose momentum

While AI-related shipments are strengthening the market, cross-border e-commerce continues to weaken.

China’s low-value and e-commerce exports declined 7% year-on-year in May, marking the sixth consecutive monthly decline.

Exports to Europe fell 15%, while shipments to Asia-Pacific declined 4%.

Although exports to the United States increased 26%, volumes remain below levels seen before the removal of the US de minimis exemption.

Xeneta suggested that part of the decline may reflect a shift from individual parcel shipments towards larger consolidated freight consignments.

Nevertheless, the overall trend indicates that e-commerce is no longer the principal growth engine for global air cargo.

Regulatory changes reshape cross-border trade

The changing regulatory landscape is also influencing international cargo flows.

From 1 July, the European Union introduced a €3 customs fee on low-value imports from outside the bloc following the removal of the €150 de minimis exemption. A further €2 handling fee is expected later this year.

In France, authorities have also moved to restrict advertising by low-cost online retail platforms including Shein, Temuand AliExpress, reflecting growing scrutiny of cross-border e-commerce.

Van de Wouw expects the industry to adjust to the new regulatory framework, much as it adapted following earlier customs changes in the United States, but reiterated that AI—not e-commerce—is now driving market growth.

Buyers favour shorter contracts amid uncertainty

Market uncertainty is also reshaping procurement strategies.

Xeneta reported that 58% of newly signed agreements between shippers and freight forwarders during the second quarter covered periods of three months or less, compared with just 22% during the same period last year.

Similarly, the proportion of chargeable weight moving through the spot market increased to 49%, up from 34% before the pandemic.

The growing preference for short-term agreements reflects continued uncertainty over future freight rates and market direction.

Van de Wouw advised shippers to avoid committing to long-term contracts while freight rates continue their gradual downward trend.

AI demand expected to sustain market—for now

Looking ahead, Xeneta believes AI-related shipments will continue supporting global air cargo demand, although the duration of the trend remains uncertain.

Previous growth drivers—including pandemic-related supply chain disruption and cross-border e-commerce—eventually lost momentum, and industry observers acknowledge that AI demand could also normalise over time.

For now, however, semiconductor and AI hardware shipments are providing the air cargo sector with a powerful new source of growth, reinforcing the importance of high-value technology supply chains in shaping the industry’s outlook for the remainder of 2026.

{kind=link}