Worldwide air cargo demand demonstrated resilience during Week 24 (June 8–14, 2026), maintaining stable volumes, capacity, and pricing despite renewed geopolitical tensions in the Middle East, according to the latest market analysis released by WorldACD Market Data.

The weekly assessment revealed that global chargeable weight increased by 1% week-on-week (WoW), highlighting the continued stability of the air freight market. While volumes declined by 5% from Central & South America (CSA) and 1% from North America, all other major regions recorded growth ranging between 2% and 4%, with the strongest performance coming from the Middle East & South Asia (MESA) region.

The temporary slowdown in North American exports largely reflected a market correction following the previous week’s sharp rebound, which was driven by the recovery of trade activity after disruptions caused by national holidays, including the US Memorial Day period. When measured on a two-week-on-two-week (2Wo2W) basis, chargeable weight from North America registered a significant 10% increase, indicating a strong recovery in demand.

On a global scale, the 2Wo2W comparison showed air cargo volumes rising by 1%, while both capacity and average pricing remained largely unchanged, underlining a balanced supply-demand environment.

Year-on-year (YoY) figures reflected robust market expansion, with worldwide chargeable weight increasing by 10%. MESA led the growth with an impressive 22% increase, followed by Africa (+14%) and Asia Pacific (+12%). Europe recorded an 8% increase, North America grew by 6%, and Central & South America reported a 2% rise compared with the same period last year.

Asia Pacific Trade Lanes Show Mixed Performance

Air cargo flows from Asia Pacific presented a varied picture. Volumes to Europe increased by 2% WoW, supported by stable exports from key manufacturing hubs including China and Japan, while Singapore recorded a 9% increase and Malaysia surged by 36% after experiencing significant declines in the preceding two weeks.

In contrast, cargo traffic from Asia Pacific to the United States declined by 2% WoW, primarily due to lower exports from Thailand, Vietnam, China, and Japan, which outweighed gains from other markets across the region.

MESA Market Remains Resilient Despite Regional Hostilities

Despite the resurgence of hostilities in the Gulf region during the week, air cargo activity from the Middle East & South Asia continued its recovery momentum. Although capacity from MESA declined by 2% WoW following a sharp 9% increase in the previous week, actual cargo volumes grew by 4%, supported largely by the post-Eid al-Adha recovery.

Traffic from MESA to Europe increased by 2% WoW, driven by strong gains from Bangladesh (+24%) and Dubai (+12%). However, exports from Sri Lanka and India fell by 14% and 6%, respectively.

Cargo flows from MESA to the United States declined marginally by 1% WoW, reflecting reduced shipments from Sri Lanka (-21%) and India (-3%). Bangladesh, however, posted a remarkable 72% rebound after experiencing a sharp decline during the previous two weeks, while Dubai recorded a 9% increase.

Freight Rates Remain Stable

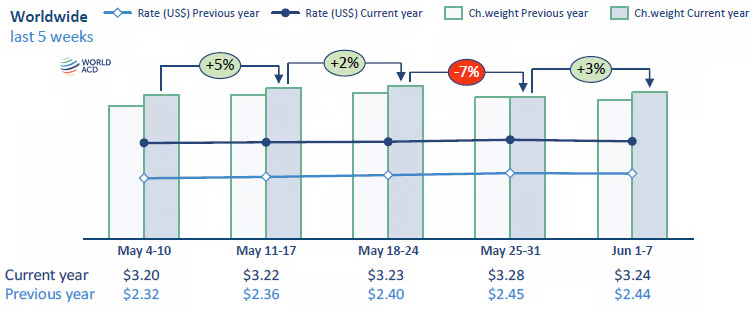

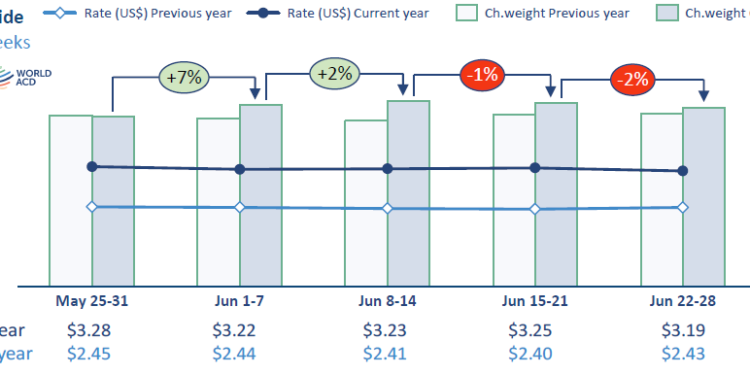

Global average air cargo pricing remained unchanged at USD 3.23 per kilogram, both on a week-on-week and two-week comparison basis, indicating a period of pricing stability after a temporary increase in Week 22.

By region, average rates increased by 1% from Europe, declined by 1% from Asia Pacific and MESA, and remained stable across other origins. On a year-on-year basis, overall pricing was significantly higher, rising by 34%, with increases ranging from 11% from Central & South America to a substantial 48% from MESA.

Spot rates from Asia to the United States continued their gradual upward trajectory, rising by 1% WoW for the fifth consecutive week since Week 20. Prices remained stable from Taiwan, Vietnam, and Indonesia, while other Asian origins recorded moderate increases, except Japan, where spot rates dropped by 12%.

Meanwhile, spot pricing from Asia Pacific to Europe remained unchanged for the third consecutive week. Higher rates from Hong Kong, China, Indonesia, and Singapore were offset by declines elsewhere, particularly Thailand, where spot prices fell by 10%.

Outlook: Improved Stability Expected if Middle East Truce Holds

According to WorldACD Market Data, the preliminary agreement between the United States and Iran aimed at ending the conflict could support a more stable operating environment in the Middle East if the agreement remains effective. A gradual restoration of passenger flight capacity through the region is expected, although a return to pre-conflict flight levels may take time.

Oil prices, which declined by approximately 5% WoW during Week 24, are also expected to ease further. However, the recovery of full oil production capacity could take several months, potentially keeping energy-related costs and freight market rates at relatively elevated levels in the near term.

The latest market trends suggest that despite geopolitical uncertainty and regional disruptions, the global air cargo industry continues to demonstrate resilience, supported by balanced capacity, steady demand, and recovering trade flows across key international corridors.

{kind=link}