Global air cargo markets are entering a phase of sustained structural pressure as rising demand from artificial intelligence and semiconductor supply chains coincides with fuel-related disruptions and reduced passenger bellyhold capacity, according to Taiwan-headquartered freight forwarder Dimerco Express Group.

The company reports that a combination of geopolitical instability in energy markets and accelerating technology-driven cargo flows is reshaping airline capacity deployment, tightening key trade lanes across Asia, Europe, and North America.

Fuel Disruptions and Reduced Belly Capacity

Dimerco highlights that the ongoing jet fuel supply pressures linked to Middle East instability have led airlines to reduce or restructure passenger services on certain routes. This has had a direct knock-on effect on bellyhold cargo availability, particularly on Asia–Europe corridors, where passenger aircraft continue to represent a significant share of total airfreight capacity.

The reduction in passenger frequency has amplified reliance on freighter aircraft, but capacity gains in dedicated cargo operations have not been sufficient to fully offset the shortfall, leading to a net tightening of available uplift.

Asia Route Volatility and Operational Disruptions

The forwarder also reported recurring operational instability across intra-Asia lanes, with frequent flight cancellations affecting services between China and destinations including Bangkok, Manila, and Jakarta. These disruptions have been attributed to a combination of localized fuel shortages and operational adjustments by airlines managing cost exposure.

Additional pressure emerged during the Labour Day holiday period in early May, when scheduled freighter services were temporarily reduced. Airlines have also implemented payload restrictions on certain routes, further limiting effective cargo capacity even where flights remain operational.

AI and Semiconductor Demand Reshaping Cargo Flows

At the same time, structural demand from high-tech sectors continues to intensify. Dimerco notes that shipments linked to artificial intelligence infrastructure, cloud computing hardware, and semiconductor production are exerting sustained pressure on global airfreight networks.

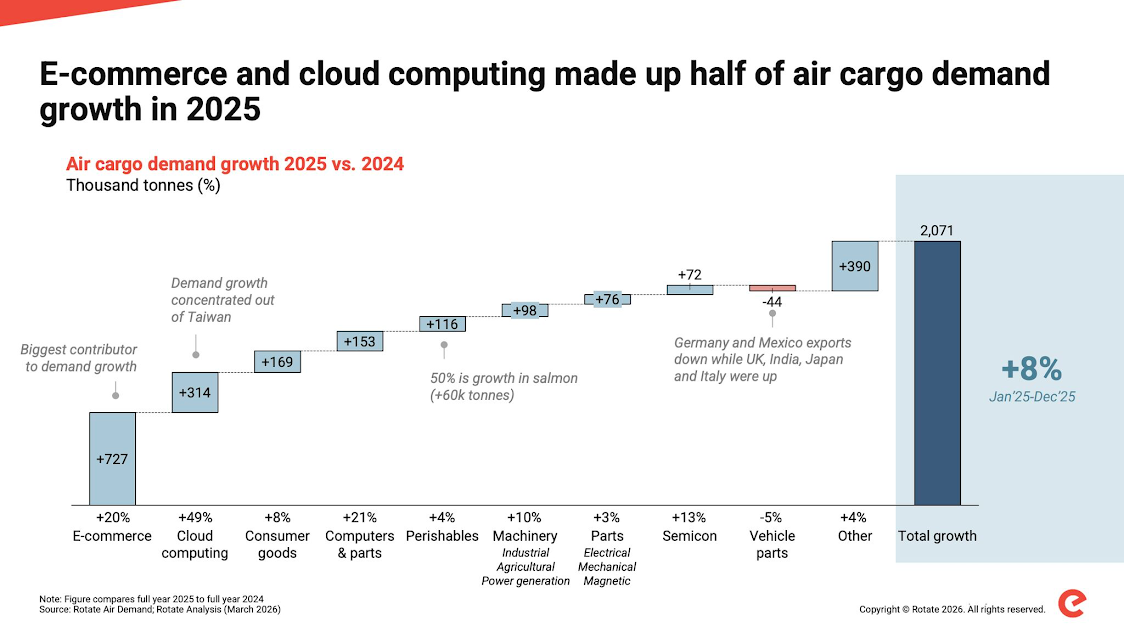

This aligns with broader industry data indicating a rapid expansion in technology-driven cargo volumes. According to market analysis by logistics data provider Rotate, airfreight volumes linked to cloud computing increased by 49% year-on-year in 2025, adding approximately 314,000 tonnes, with growth heavily concentrated in exports from Taiwan.

The only category exceeding this expansion was e-commerce, which grew by 727,000 tonnes, or 20% compared with 2024 levels, reinforcing the dual structural drivers of digital consumption and digital infrastructure development in global air cargo demand.

Rotate noted that “with e-commerce showing no signs of slowing, and AI infrastructure buildouts accelerating, the capacity squeeze may only tighten.”

Taiwan and North Asia Under Pressure

Dimerco highlighted particularly tight conditions on transpacific routes, with capacity constraints on both direct and indirect services from Taipei to the United States. Strong demand from electronics and semiconductor shippers has contributed to persistent upward pressure on rates, with urgent cargo frequently securing uplift at premium pricing.

General cargo, by contrast, is increasingly being routed through indirect services due to limited availability on direct flights.

The situation is mirrored in South Korea, where reduced airline supply and strong outbound demand—particularly from e-commerce and technology sectors—have resulted in “severe space constraints and rising rates.” The imbalance is especially pronounced on routes to the United States and Southeast Asia, where semiconductor and IT-related shipments continue to dominate available capacity.

Market Behaviour Shifts as Shippers Plan Earlier

Kathy Liu, Vice President of Global Sales and Marketing at Dimerco Express Group, noted that the tightening market conditions are forcing structural changes in shipper behaviour.

“Demand for traditional commodities is still relatively stable, but cost pressure is building across the board,” Liu said. “With fuel surcharges rising and capacity tightening, shippers are having to plan earlier and manage costs much more carefully than before.”

Her assessment aligns with wider industry sentiment, with forwarders increasingly reporting earlier booking cycles, greater reliance on contract allocations, and a shift toward longer-term capacity planning as volatility persists.

Airlines Expected to Rationalise Capacity

Market participants expect airlines to continue adjusting network structures in response to profitability pressures and operational constraints. Analysts suggest that lower-yield routes are likely to face frequency reductions first, while high-frequency services may also be scaled back if fuel costs and capacity imbalances persist.

As noted by industry observers, any reduction in scheduled flights—particularly passenger services—will directly impact bellyhold availability, further tightening already constrained cargo lanes.

Structural Outlook: Capacity Squeeze Deepens

The convergence of energy market instability, geopolitical disruption, and accelerating AI-driven demand has created a complex operating environment for airfreight stakeholders. While traditional commodity flows remain broadly stable, the structural shift toward high-value, high-priority technology shipments is reshaping global capacity allocation.

With semiconductor production, AI infrastructure development, and cross-border e-commerce continuing to expand, forwarders anticipate sustained pressure on key Asia-origin lanes and transpacific corridors well into the medium term.

{kind=link}