WorldACD Data Shows Resilient Freight Volumes, Rising Spot Rates and Gradual Capacity Recovery Despite Ongoing Middle East Disruptions

The global air cargo market showed signs of stabilisation in mid-May 2026 as demand recovered following the seasonal “Golden Week” holidays in East Asia and supply chains continued to face pressure from geopolitical disruptions. According to the latest WorldACD Market Data, cargo volumes remained resilient, rates stayed elevated, and capacity recovery continued at a gradual pace despite persistent challenges linked to the conflict in the Middle East. Industry analysts suggest that constrained ocean freight capacity, longer shipping lead times and inventory stockpiling are continuing to support air cargo demand across major trade lanes.

Air Cargo Demand Remains Resilient Following Seasonal Slowdown

Global air cargo markets appear to have entered a phase of relative stability after navigating a turbulent start to the second quarter of 2026. According to the latest weekly figures from WorldACD Market Data covering the five-week period ending May 24, worldwide air freight volumes remained broadly unchanged during Week 21 (May 18–24) compared with the previous week.

While tonnage growth was flat on a week-on-week basis, global chargeable weight remained approximately 2% higher than during the corresponding week in 2025, reflecting the continued resilience of international trade flows despite ongoing geopolitical uncertainty and operational disruptions.

The recovery follows the seasonal slowdown associated with the “Super Golden Week” holiday period across several East Asian economies earlier in May. Market conditions have since normalised, allowing cargo demand to regain momentum, particularly on Asia-origin routes.

Industry experts point to growing supply chain pressures in Europe and North America as a key factor supporting air cargo demand. Shipping lead times have reached their highest levels in several months due to continued maritime disruptions linked to regional conflicts, prompting many shippers to accelerate inventory replenishment through air freight solutions.

As a result, cargo volumes originating from the Asia-Pacific region during Week 21 were approximately 5% higher than the same period last year, underscoring the region’s continued role as the primary engine of global air cargo growth.

Middle East Disruptions Continue to Reshape Market Dynamics

Despite signs of recovery across most major regions, the impact of ongoing geopolitical tensions in the Middle East continues to weigh heavily on global air cargo networks.

The Middle East and South Asia (MESA) region recorded a modest 2% increase in chargeable weight compared with the previous week, indicating improving market activity despite operational challenges. However, cargo volumes remained 1% below year-earlier levels, highlighting the lingering effects of reduced connectivity and capacity limitations.

The ongoing conflict has significantly altered established trade flows, forcing airlines and freight forwarders to redesign routes, adjust schedules and seek alternative gateways to maintain service continuity.

Market observers note that while cargo demand remains strong, capacity shortages in key Gulf hubs continue to restrict the region’s ability to fully capitalise on available market opportunities.

Freight Rates Remain Elevated Amid Tight Capacity

Air cargo pricing remained firm throughout the reporting period, supported by constrained capacity and sustained demand.

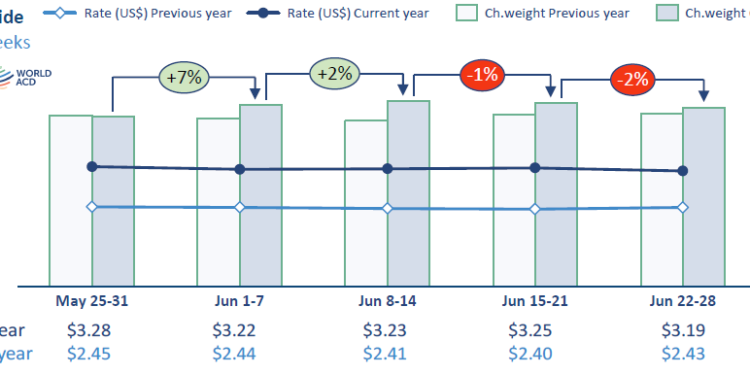

WorldACD data shows that average global air freight rates remained unchanged week-on-week at US$3.23 per kilogram during Week 21. However, compared with the same period in 2025, average rates were 35% higher.

The increase reflects several market factors, including reduced capacity availability, significantly higher fuel costs and increased reliance on freighter aircraft as airlines seek to compensate for operational disruptions affecting passenger belly-hold capacity on certain routes.

The continued strength in pricing indicates that market fundamentals remain favourable for cargo carriers, even as economic uncertainty and geopolitical risks persist.

Spot Market Strength Highlights Ongoing Demand Pressure

The spot market continued to outperform broader contract pricing trends, providing further evidence of sustained demand and tight capacity conditions.

Global spot rates increased by an additional 1% week-on-week during Week 21, reaching an average of US$3.75 per kilogram.

The strongest gains were recorded from Africa, where spot rates rose by 4%, while Asia-Pacific rates increased by 2% to US$5.16 per kilogram.

Based on more than 500,000 weekly market transactions monitored by WorldACD, average global spot rates are now approximately 50% higher than a year ago.

The Middle East and South Asia region recorded some of the most significant pricing increases, with spot rates climbing 59% year-on-year to US$4.26 per kilogram.

Most other major regions also registered year-on-year spot rate growth exceeding 40%, reflecting widespread capacity constraints and robust demand. Central and South America represented the only notable exception, where spot rates increased by a comparatively moderate 18% over the same period.

Passenger Capacity Drives Recovery

On the supply side, global air cargo capacity continued its gradual recovery trajectory during Week 21.

Worldwide capacity increased by approximately 1% compared with the previous week, driven primarily by growth in passenger aircraft capacity, which rose by 2%. Freighter capacity remained largely unchanged.

The gradual return of passenger services is helping restore additional belly-hold capacity to the market, although recovery remains uneven across regions.

The most significant week-on-week increase occurred within the Middle East and South Asia region, where available capacity improved by 5%.

However, despite recent gains, capacity levels remain significantly below pre-conflict benchmarks.

Compared with Week 7 of 2026, prior to the escalation of military tensions involving Iran, overall capacity to and from the Middle East and South Asia region remains approximately 32% lower.

The situation is even more pronounced in the Gulf region, where available air cargo capacity is currently around 48% below pre-war levels.

Industry analysts note that these figures illustrate the continuing difficulty carriers face in rebuilding operations amid an uncertain geopolitical environment. While airlines outside the region have increased freighter deployments to offset some of the lost capacity, restoring previous network levels remains a complex challenge.

Global Capacity Growth Slows Compared with Early 2026

Compared with the same week last year, global air cargo capacity was approximately 3% higher during Week 21.

Although positive, the figure represents a substantial slowdown from the stronger growth rates recorded during the opening months of 2026.

Prior to the outbreak of conflict involving Iran and the resulting disruptions across the Gulf region, worldwide capacity expansion was running at more than double current levels.

The decline highlights the significant influence that geopolitical developments continue to exert on global air cargo operations and network planning.

Outlook: Stability Amid Continuing Uncertainty

While market conditions remain volatile, the latest WorldACD data suggests that global air cargo is entering a period of relative equilibrium.

Demand fundamentals remain healthy, supported by strong Asia-linked trade flows, inventory restocking activity and longer ocean freight transit times. At the same time, elevated freight rates continue to reflect ongoing supply constraints and operational complexity.

Looking ahead, the industry’s ability to sustain growth will largely depend on how effectively carriers adapt to changing geopolitical conditions, manage rising operating costs and restore capacity on disrupted trade corridors.

For now, the market appears to have found a degree of stability, but uncertainty surrounding global conflicts, fuel prices and trade patterns means that air cargo operators will need to remain agile as they navigate the remainder of 2026.

{kind=link}