Global airfreight markets continue to face capacity constraints despite increasing available space, as strong demand from Asia-Pacific technology, semiconductor and e-commerce sectors keeps pressure on capacity and pricing, according to the latest Air & Ocean Lens market update from DHL Global Forwarding (DGF).

In its newsletter published on 22 June, DHL Global Forwarding noted that although global air cargo capacity increased by 2% year-on-year in May, the additional capacity has not been sufficient to balance the market, particularly across high-demand long-haul trade corridors.

“Capacity is growing, but not at a pace or in a way that relieves market pressure,” DGF stated, highlighting that airlines are selectively deploying capacity towards routes offering stronger yields, while global passenger bellyhold capacity declined by 3% year-on-year.

Asia-Pacific Continues to Drive Global Air Cargo Growth

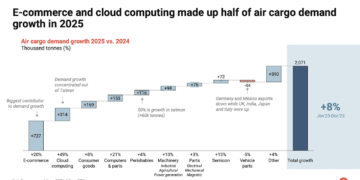

Air cargo demand expanded by 5% year-on-year in April and remains 4% higher year-to-date, with Asia accounting for approximately half of worldwide air freight volumes.

The region has recorded 8% growth over the same period, supported by rising shipments of high-value products such as semiconductors, artificial intelligence (AI) infrastructure components and advanced technology equipment.

According to DHL Global Forwarding, the increasing movement of technology-related cargo has reinforced Asia-Pacific’s importance across premium air cargo trade lanes.

Niki Frank, Chief Executive Officer of DHL Global Forwarding Asia Pacific, said:

“Asia-Pacific is not only powering global trade but increasingly shaping the pace, direction and capability of international supply chains.”

The continued imbalance between robust demand and constrained supply is also reflected in air freight pricing. Global spot rates remain at around USD 3.67 per kilogram, representing a 48% increase compared with the previous year, driven by strong demand and elevated operating costs.

Airlines Maintain Focus on High-Yield Routes

DHL expects Asia-Pacific air cargo demand to remain resilient in the coming months, supported by continued expansion in e-commerce, technology manufacturing and supply chain diversification strategies.

However, capacity growth is likely to remain measured, as airlines continue to prioritise high-yield international routes rather than broadly increasing available capacity.

This dynamic suggests that airfreight rates are likely to remain elevated until demand conditions soften or additional capacity enters the market at a meaningful scale.

Ocean Freight Faces Early Peak Season Pressures

In the maritime sector, DHL Global Forwarding reported that the traditional peak shipping season has arrived earlier than expected, placing further strain on already constrained ocean freight capacity.

Shippers are accelerating shipments and securing additional space ahead of anticipated increases in bunker adjustment factors, which are scheduled to take effect from 1 July. The strategy is intended to reduce the risk of cargo rollovers and supply chain disruptions.

Despite continued growth in nominal vessel capacity, operational challenges such as port congestion, longer transit times and vessel rerouting are significantly reducing effective capacity.

DGF estimates that approximately 17% of usable ocean freight capacity has been removed from the market due to these disruptions.

Commenting on market conditions, Niki Frank said:

“Peak season is arriving earlier and with greater intensity, compressing cargo volumes into shorter periods and creating immediate pressure on capacity and freight rates.”

DHL Global Forwarding expects that a significant decline in freight rates is more likely to result from weaker demand rather than a rapid recovery in available capacity, as both air and ocean supply chains continue to face operational and geopolitical challenges.

{kind=link}