Global air cargo markets are showing early signs of stabilisation as capacity gradually returns to Middle East and South Asia (MESA) trade lanes, following weeks of volatility triggered by military tensions in the region. According to the latest weekly market assessment covering the period from 13 to 19 April 2026, the pace of air freight rate increases has slowed significantly, even as year-on-year pricing remains elevated due to earlier supply chain disruptions.

Rate Growth Moderates After Sharp Rally

Average global spot rates rose marginally by 1% week-on-week to US$3.73 per kilogram in Week 16, marking the smallest weekly increase recorded since the onset of the conflict-driven disruption in late February. Despite the slowdown, rates remain 46% higher year-on-year and over 40% above late February levels, when regional instability first intensified.

The modest increase was primarily driven by Asia Pacific origins, where spot rates rose 3% week-on-week to US$5.14 per kilogram. In contrast, rates from MESA origins declined by 2% week-on-week to US$4.74 per kilogram, although they remain significantly elevated at 67% above the same period last year.

Capacity Recovery Underway in Key Trade Lanes

Global air cargo capacity remained broadly stable week-on-week, as gains in freighter operations offset reductions in bellyhold capacity, the latter influenced by operational disruptions in Europe, including industrial action in Germany and intermittent flight adjustments linked to fuel supply constraints.

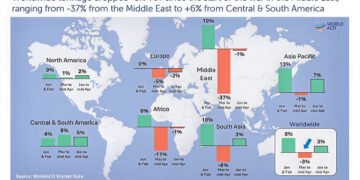

More notably, capacity from MESA origins increased by approximately 7% week-on-week, narrowing the region’s overall capacity deficit from 35% in the previous week to 30%. The recovery was most pronounced in Gulf markets, where the deficit improved from 53% to 46%, while the Levant region also recorded a notable improvement, narrowing from 29% to 20%.

South Asia has now largely returned to near-normal operational levels, with capacity only 4% below pre-conflict benchmarks. Globally, overall capacity stands just 6% below pre-war levels, indicating a gradual rebalancing of supply conditions.

Diverging Trends in Demand and Tonnage

Despite improving capacity conditions, air cargo tonnages from MESA origins declined by 6% week-on-week, reflecting continued market volatility and uneven recovery across key trade lanes.

Exports from India fell by 4% and Sri Lanka by 14%, while Dubai-origin shipments increased by 8%, partially offsetting regional declines. Trade flows from MESA to Europe decreased by 3% week-on-week, while shipments to the United States declined marginally by 1%.

Spot rates on major corridors also softened. MESA–Europe rates fell 5% week-on-week, though they remain 82% higher year-on-year. MESA–US pricing declined 4% week-on-week but continues to show a strong 64% year-on-year increase, reflecting sustained demand pressure despite recent easing.

Post-Holiday Rebound Supports Global Volumes

Globally, air cargo tonnages rebounded 3% week-on-week, driven largely by post-holiday recovery in Europe (+11%) and Central & South America (+9%), with additional gains in North America (+3%). This was partially offset by declines in MESA and African origins, the latter down 4% week-on-week amid ongoing regional challenges.

Mixed Performance Across Asia Pacific Trade Lanes

Asia Pacific markets, which played a key role in supporting global rate stability, showed mixed performance. Spot rates to Europe increased slightly by 1% week-on-week, driven by stronger pricing from South Korea and Thailand, while volumes declined 3%.

On the transpacific route, Asia Pacific–US rates remained stable, with gains from Northeast Asia offset by weaker pricing from Southeast Asia. Volumes on this corridor increased marginally by 1%, reflecting balanced but cautious demand conditions.

Market Outlook

While the partial ceasefire in the Middle East has introduced a degree of operational stability, industry conditions remain highly sensitive to geopolitical developments, particularly around key maritime chokepoints and aviation corridors. Capacity restoration continues, but demand-side volatility and uneven regional recovery suggest that air cargo markets are likely to remain cautiously balanced in the near term.

{kind=link}