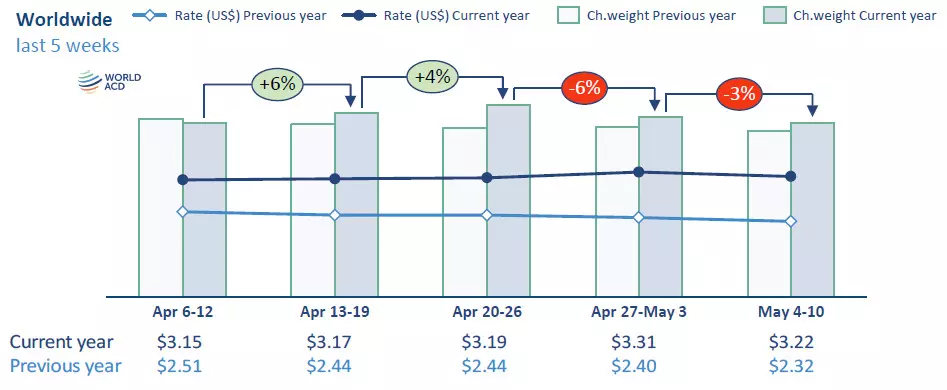

Global air cargo markets softened in the first full week of May as holiday-driven demand in Asia subsided and the seasonal surge in flower shipments for Mother’s Day came to an end, leading to declines in tonnage, pricing, and available capacity across several major trade lanes.According to the latest weekly market analysis from WorldACD, global air freight volumes fell 3 percent week on week during Week 19, with the combined performance of Weeks 18 and 19 showing a 6 percent decline compared with the previous two-week period. The analysis is based on more than 500,000 weekly shipment transactions monitored across global air cargo markets.Despite the short-term slowdown, annual comparisons remain positive, highlighting continued structural strength in international air freight demand.

Holiday Effects Hit Asia and Flower Exports

The largest week-on-week declines were recorded in Asia Pacific and Central and South America, both of which had benefited from seasonal cargo peaks in previous weeks.Chargeable weight from Asia Pacific fell 5 percent week on week and was down 8 percent over the two-week period, largely reflecting the end of “Super Golden Week,” the holiday period that combines Japan’s Golden Week with national holidays in China and South Korea.Outbound cargo from Central and South America declined even more sharply, falling 19 percent week on week as Mother’s Day flower exports wound down. Over the two-week comparison period, the region recorded a 9 percent drop.The Middle East and South Asia (MESA) region also posted weaker volumes, with tonnage down 4 percent week on week.By contrast, Europe and North America recorded modest gains of 2 percent and 5 percent respectively, supported by a rebound in post-holiday demand from Asian markets.On a year-on-year basis, global tonnage remained 5 percent above 2025 levels, with all origin regions reporting growth except Africa, which declined 11 percent.

Asia–US Trade Remains Strong Despite Weekly Correction

The holiday effect was especially visible on outbound Asia traffic to Europe and the United States, where volumes declined 9 percent week on week.Japan saw some of the steepest drops, with cargo volumes down:44 percent to the United States54 percent to EuropeHowever, underlying demand remains resilient in key manufacturing markets.Vietnam stood out as a positive performer, with exports to Europe rising 22 percent week on week, supported by continued demand for electronics, textiles, and industrial shipments.Year-on-year data also underscores the resilience of Asia–US trade lanes:Asia Pacific to US volumes rose 33 percentShipments from China and Hong Kong to the US climbed nearly 50 percentMeanwhile, Asia–Europe volumes slipped 1 percent year on year due to lower exports from Japan, Indonesia, and Hong Kong.

MESA Market Shows Mixed Dynamics

Cargo flows from MESA to both Europe and the United States declined 5 percent week on week, though underlying market performance varied significantly by origin.

Traffic to Europe weakened due to double-digit declines from Dubai and Bangladesh.

By contrast, shipments from Dubai to the United States surged 65 percent after a sharp decline the previous week.

Exports from:

India fell 7 percent

Sri Lanka declined 5 percent

Year-on-year, MESA volumes remained robust:

Up 11 percent to the US

Down 1 percent to Europe

Overall regional growth of 6 percent

Pricing Softens but Remains Significantly Above 2025

As demand eased, global air freight pricing also moved lower.Average worldwide rates declined 3 percent week on week to US$3.22 per kilogram, mirroring the drop in global chargeable weight.Regional pricing trends showed:Central and South America: down 8 percentAfrica: down 7 percentEurope: up 1 percentNorth America: flatThe decline in Latin America again reflected the end of seasonal flower exports.Despite weekly corrections, annual pricing remains elevated.WorldACD data shows:Global average rates up 39 percent year on yearSpot rates up 51 percentAmong all regions, MESA continues to record the strongest pricing performance.Spot rates from MESA:To the US rose 60 percent year on yearTo Europe rose 72 percent year on yearDubai led these increases, with spot rates rising:135 percent to the US181 percent to Europe

Capacity Contracts as Seasonal Peaks End

Global air cargo capacity also declined as carriers adjusted schedules following the end of seasonal demand peaks.Available capacity fell 2 percent week on week after remaining flat in Week 18.Regional changes included:Central and South America: down 4 percentAsia Pacific: down 3 percentNorth America: down 2 percentAfrica: down 2 percentCapacity from Europe and MESA remained largely unchanged, suggesting that growth in those regions may be stabilizing.Industry analysts note that while freighter operations from Gulf carriers have largely recovered, passenger bellyhold capacity in the Middle East remains constrained by ongoing geopolitical uncertainty.

Rising Fuel Costs Trigger Schedule Adjustments

Airlines are also facing mounting operational pressure from elevated fuel prices.Industry data indicates carriers have cut approximately 13,000 flights in May, primarily on short-haul regional routes operated by narrowbody aircraft.While the immediate impact on dedicated cargo capacity remains limited, analysts expect additional network adjustments if fuel costs remain elevated throughout the second quarter.For now, the latest figures suggest that while seasonal peaks have passed, underlying air cargo fundamentals remain strong, particularly across Asia–US and Middle East export corridors, where both pricing and annual demand continue to outperform last year’s levels.

{kind=link}